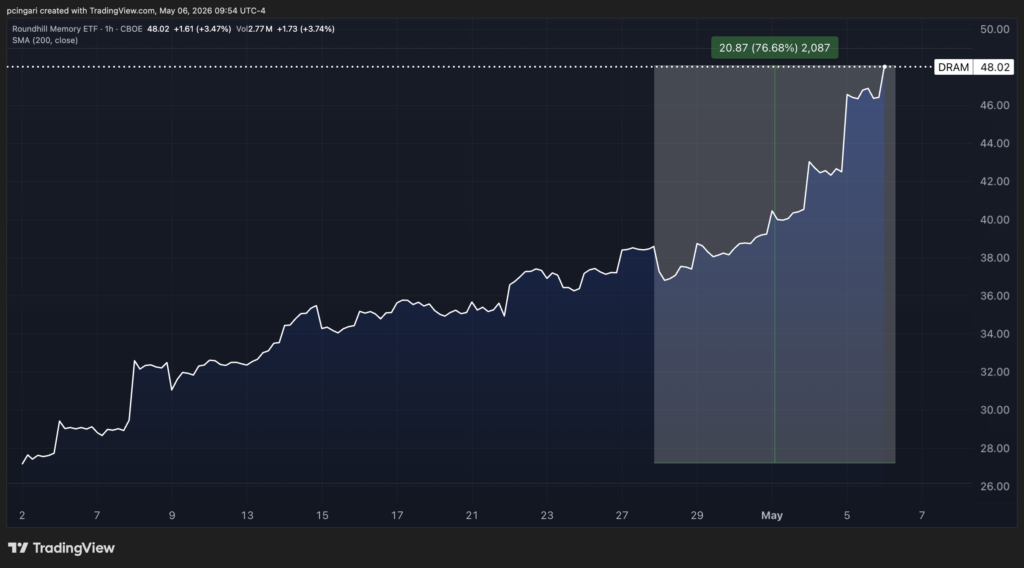

An exchange-traded fund that did not exist five weeks ago has just become the loudest signal in the entire AI infrastructure trade.

The Roundhill Memory ETF (CBOE: DRAM) — the first U.S.-listed fund offering pure-play exposure to global memory semiconductor companies — has rallied over 70%, a month after Roundhill Investments brought it to market on April 2.

Inflows tell a similar story. The fund crossed $1 billion in assets in 10 trading days, and Dave Mazza, chief executive officer of Roundhill Investments, told Benzinga that DRAM has now pulled in over $2.5 billion since inception.

A Gap In The Market, Not Just A Theme

“The strong returns since inception validated our thesis that memory chips are the most critical and supply-constrained layer of the AI infrastructure buildout, and the companies making them were being systematically undervalued,” Mazza said.

The performance, in his telling, is not the reason the money showed up. The product structure is.

Before DRAM, an investor wanting concentrated exposure to memory had two imperfect options: a South Korean ETF – such as the iShares South Korea ETF (NYSE:EWY) – that bundled chipmakers with conglomerates, banks, and consumer companies, or a broad semiconductor ETF – like the iShares Semiconductor ETF (NYSE:SOXX) – where memory names sat as a small slice of the portfolio.

“DRAM was built to solve that problem by offering pure-play exposure to the global memory complex in an ETF,” Mazza said.

The white space was real. Memory has spent the last eighteen months going from a commodity backwater to one of the tightest links in the AI supply chain, and there was no clean way to own it.

What’s Inside The Fund

DRAM holds nine names. Three of them — Micron Technology Inc. (NASDAQ:MU), SK hynix, and Samsung Electronics Co. — account for roughly 69% of the portfolio.

The remaining weight is spread across Sandisk Corp. (NASDAQ:SNDK), Seagate Technology Holdings PLC (NASDAQ:STX), Kioxia Holdings, Western Digital Corp. (NASDAQ:WDC), Nanya Technology, and Winbond Electronics.

| DRAM ETF Holding | Weight |

|---|---|

| Micron Technology Inc. | 26.77% |

| SK hynix | 23.75% |

| Samsung Electronics Co. | 18.55% |

| Sandisk Corp. | 6.10% |

| Seagate Technology Holdings PLC | 5.28% |

| Kioxia Holdings | 5.27% |

| Western Digital Corp. (NASDAQ:WDC) | 4.68% |

| Nanya Technology | 3.13% |

| Winbond Electronics | 1.63% |

That concentration is not a flaw, in Mazza’s view. It is the point.

Nine Stocks Is The Industry, Not An Oversight

“The precision is intentional. DRAM was designed to give investors targeted exposure to the memory theme,” Mazza said.

“The nine holdings reflect the reality of the industry as the global memory market is concentrated, with three companies controlling the vast majority of HBM production.”

HBM stands for high-bandwidth memory — the stacked chips that sit next to AI accelerators and feed them data fast enough to keep up.

Micron, SK hynix, and Samsung are the three names that matter. There is no fourth.

“The barriers in the memory industry are extraordinary and often underappreciated,” Mazza said, citing the tens of billions in capital, years of construction time, and constrained access to ASML’s EUV lithography machines that have kept the oligopoly intact for decades.

China is the most frequently cited threat, but Chinese manufacturers remain multiple generations behind on HBM specifically — the highest-margin, most AI-critical layer — and closing that gap runs into both process development and export controls.

Who’s Actually Buying The DRAM ETF

The investor mix has been broader than typical thematic launches.

Mazza said both U.S. and non-U.S. retail investors have embraced the product, and that the breadth of geographic interest “speaks to how broadly the memory thesis has resonated.”

Korean retail flows have been particularly visible. According to Seoul Economic Daily, Korean retail investors trading U.S. equities — known locally as Seohak Ants — bought roughly 10% of the inflows into DRAM in its first month, an unusually high foreign-retail share for a U.S.-listed thematic fund.

Institutional adoption is showing up too, particularly through derivatives.

“We’re also seeing institutional investors use the product in various ways, particularly due to its robust options volume,” Mazza said.

Options volume on a one-month-old ETF that already averages over 11,000 contracts traded per day is not a retail signature — that is funds expressing views on the memory cycle through DRAM rather than building single-name positions.

Not A Cycle, A Re-Rating

The most consequential part of the conversation was Mazza’s framing of where memory goes from here. He rejects the cyclical lens entirely.

“We think the framing of the memory cycle is increasingly the wrong lens as we are seeing a structural shift, not a cyclical upturn,” Mazza said.

“Hyperscalers are signing multi-year committed contracts. For example, Micron signed its first-ever five-year strategic customer agreement this year.”

The detail matters.

Memory has historically been a boom-and-bust business priced like a commodity, with one-year long-term agreements and aggressive spot-market swings. Five-year contracts on both volume and price, signed with hyperscalers, are a different animal.

They convert what used to be a swing-trade industry into something closer to contracted infrastructure — a regime more like utilities or industrial gases than DRAM-as-it-was.

That is the crux of the bull case Mazza is selling.

“The question is not when the cycle turns, but when the market re-rates these businesses to reflect their new reality as contracted infrastructure suppliers. We think that the re-rating cycle still has significant room to run,” Mazza said.

Photo: Shutterstock

Recent Comments