The Headline Said 1.0 Bid to Cover. The Fine Print Is Saying Something Very Different.

Headline vs Reality

Germany’s Debt Management Office targeted €6 billion of sales for a new 10-year Bund auction this week. The official bid/cover ratio printed 1.0- Looks okay, right?

It’s actually worse. Much worse.

Here’s the trick: Germany calculates bid/cover as bids divided by what was sold, not bids divided by the announced target (which is how it’s calculated in America). So if barely anyone shows up to buy the debt, they just sell less, and the ratio stays around 1, by construction. The denominator shrinks to match the numerator.

Because of this, this math literally cannot print below 1.0

The honest number, which is total bids divided by what was offered was 0.67x. The total bids came in at €4bn against a €6bn target. In any other sovereign debt market, that’s a failed auction. In Germany, it gets rebranded as “market smoothing.”

What the Bids Actually Looked Like

But wait, it gets worse….

Of the €4bn in bids, only €2.15bn were “competitive“- this means price-sensitive demand that actually has an opinion on the price they pay (therefore, the yield they’re willing to accept).

The other €1.87bn was “non-competitive”; primary dealers fulfilling their obligations at whatever the average price turned out to be, with no view expressed. Real price-discovering demand covered just 36% of the €6bn target.

Germany retained 35% of the announced deal: €2.1bn went straight to the Bundesbank’s “market smoothing” account instead of to bond buyers. Normally retention is a deliberate tactical choice of 15–20%, held back to maintain secondary market liquidity. But at 35%, it wasn’t a choice. It was the unsold portion (“retained”) wearing a euphemism, as only a government can do

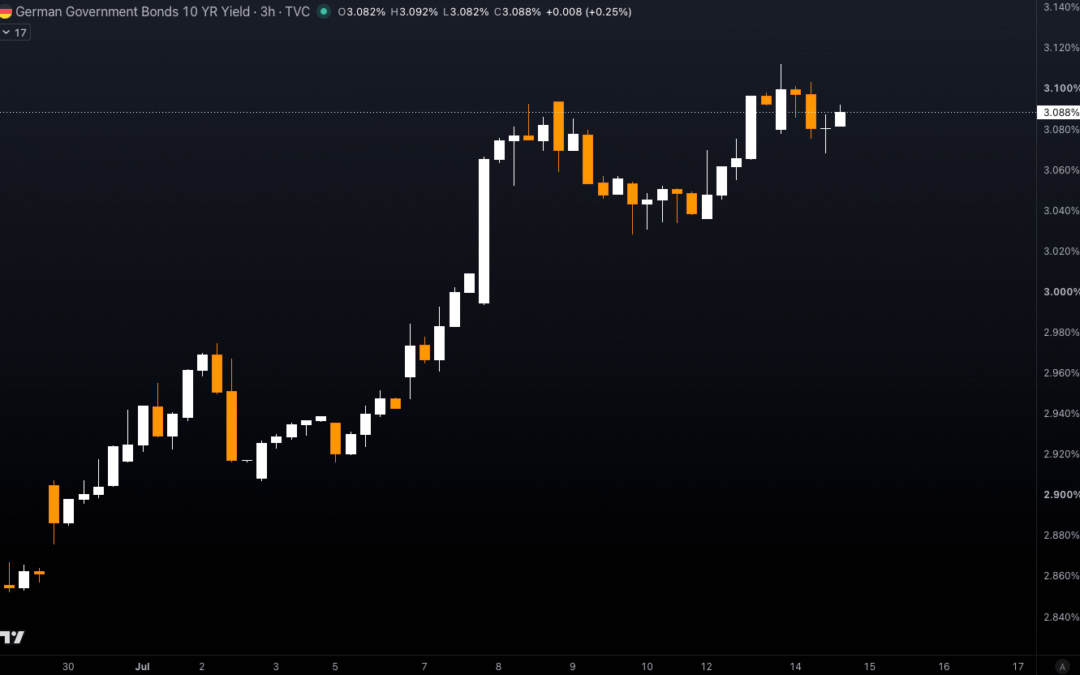

The clearing price came in at 3.09% (bond auctions are conducted in the style of a “Dutch Auction”)- the highest coupon on a new 10-year Bund since the GFC era. Germany spent a decade issuing at negative yields. Now it’s paying 3%+ and still can’t find demand

Why It May have Happened Now

The timing of this matters. This auction hit the tape the same morning Trump declared the Iran ceasefire “over” at the NATO summit in Turkey. Brent crude oil soared over 6% to $78, which hit global sovereign debt hard: the 10-year Bund yield added nearly 9 basis points on the day, UK gilt yields were up +10bp, France and Italy approaching +13bp.

The ECB’s Isabel Schnabel warned that the conflict’s economic impact persists while core inflation remains elevated, and ECB rate-hike bets started moving. Primary dealers (the buyer of last resort, with agreements to buy unwanted debt) were being asked to underwrite a €6bn new issue immediately during this global sovereign debt sell-off

The rational response wasn’t to cancel the auction, but to step back and let the ‘retention’ mechanism absorb the damage.

The Supply Problem Doesn’t Stop Here

This is where it gets really important to understand, because this auction might be just the beginning.

There are already six more ‘reopenings’ of this exact bond (ISIN number) scheduled through the end of November, totaling another ~€33.5bn. Plus the Bundesbank is sitting on today’s €2 billion retention that still needs to find a buyer in the secondary market on top of that. This single ISIN is headed for roughly €39.5bn outstanding by year-end.

And that’s just one bond. Germany has 15 ten-year auctions this year alone, totaling €82bn. The government just approved a 2027 budget with borrowing raised to €203.6bn (mainly a defense spending bumb), which is up from €196.5bn just a few months ago.

The sovereign debt supply is accelerating at the exact moment that the demand side is clearly thinning.

But it Gets Even Worse

Yep, it gets worse…. this isn’t just a German story. It’s part of the same global government debt sell-off/repricing that’s been playing out across every major sovereign debt market.

Japanese life insurers and pension funds which have historically been some of the largest marginal buyers of global duration (long-duration debt, like 10yr+) are repatriating capital back home to Japan, as JGB yields finally offer something real (compared to decades of negative rates). Sovereign duration demand is fungible-

When it’s absent in Japan, it shows up as thinner bids at Bund auctions in Germany and Gilt auctions in London. The global financial system is incredibly interconnected

What we’re watching in real time is the unwind of the post-GFC/ZIRP era where central banks spent a decade suppressing yields but are now facing a world where the private market doesn’t want to absorb the supply at anything close to the old prices (yields).

What it Means

Germany doesn’t “fail” bond auctions. But only because the system was specifically designed to prevent that from ever happening. But the Bundesbank quietly buying a third of its own government’s debt and calling it market smoothing is, for all intents and purposes, failed auctions.

The country that once issued 10-year debt at negative yields is now paying 3%+ and still needs its central bank to sweep up the unwanted debt. Meanwhile, the government debt supply is only growing, and real money is clearly demanding more yield (lower prices) to show up, and the global bid for long-duration government debt is structurally a lot thinner than it’s been in years.

Every round of central bank absorption, whether it’s the Bundesbank smoothing a “retention” or the Fed doing “Reserve Management Purchases”, is just another form of the same thing: institutions printing to paper over what the market won’t buy at current prices.

Bitcoin.

Recent Comments