In today’s fast-paced and highly competitive business world, it is crucial for investors and industry followers to conduct comprehensive company evaluations. In this article, we will delve into an extensive industry comparison, evaluating AT&T (NYSE:T) in relation to its major competitors in the Diversified Telecommunication Services industry. By closely examining key financial metrics, market standing, and growth prospects, our objective is to provide valuable insights and highlight company’s performance in the industry.

AT&T Background

The wireless business contributes nearly 70% of AT&T’s revenue. The company is the third-largest US wireless carrier, connecting 74 million postpaid and 17 million prepaid phone customers. Fixed-line enterprise services, which account for about 14% of revenue, include internet access, private networking, security, voice, and wholesale network capacity. Residential services, about 11% of revenue, primarily consist of in-home broadband internet access, serving 15 million customers. AT&T also has a sizable presence in Mexico, with 25 million wireless customers, but this business only accounts for 3% of revenue. The company recently sold its 70% equity stake in satellite television provider DirecTV to its partner, private equity firm TPG.

| Company | P/E | P/B | P/S | ROE | EBITDA (in billions) | Gross Profit (in billions) | Revenue Growth |

|---|---|---|---|---|---|---|---|

| AT&T Inc | 7.11 | 1.34 | 1.19 | 3.45% | $12.18 | $18.94 | 2.87% |

| Verizon Communications Inc | 10.35 | 1.72 | 1.29 | 4.86% | $13.62 | $20.77 | 2.85% |

| Comcast Corp | 4.55 | 0.94 | 0.68 | 2.35% | $7.69 | $20.57 | 5.25% |

| BCE Inc | 4.50 | 1.41 | 1.15 | 3.09% | $2.71 | $4.21 | 4.01% |

| TELUS Corp | 24.73 | 1.49 | 1.13 | 0.87% | $1.58 | $3.13 | -0.58% |

| Tutor Perini Corp | 51.71 | 3.27 | 0.71 | 2.11% | $0.08 | $0.15 | 11.46% |

| Uniti Group Inc | 2.45 | 8.28 | 1.09 | -24.51% | $0.41 | $0.6 | 236.0% |

| IDT Corp | 18.39 | 4.17 | 1.18 | 6.2% | $0.03 | $0.12 | 4.55% |

| Average | 16.67 | 3.04 | 1.03 | -0.72% | $3.73 | $7.08 | 37.65% |

When analyzing AT&T, the following trends become evident:

-

With a Price to Earnings ratio of 7.11, which is 0.43x less than the industry average, the stock shows potential for growth at a reasonable price, making it an interesting consideration for market participants.

-

With a Price to Book ratio of 1.34, significantly falling below the industry average by 0.44x, it suggests undervaluation and the possibility of untapped growth prospects.

-

With a relatively high Price to Sales ratio of 1.19, which is 1.16x the industry average, the stock might be considered overvalued based on sales performance.

-

The Return on Equity (ROE) of 3.45% is 4.17% above the industry average, highlighting efficient use of equity to generate profits.

-

The Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) of $12.18 Billion is 3.27x above the industry average, highlighting stronger profitability and robust cash flow generation.

-

The company has higher gross profit of $18.94 Billion, which indicates 2.68x above the industry average, indicating stronger profitability and higher earnings from its core operations.

-

The company’s revenue growth of 2.87% is significantly lower compared to the industry average of 37.65%. This indicates a potential fall in the company’s sales performance.

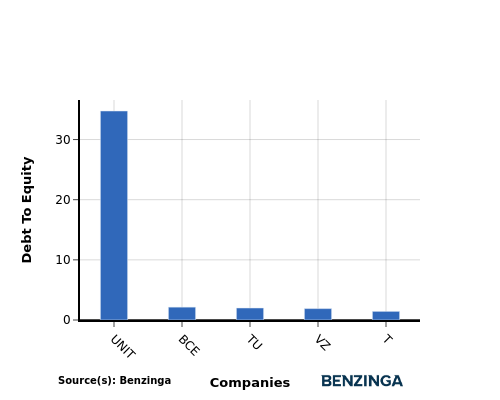

Debt To Equity Ratio

The debt-to-equity (D/E) ratio measures the financial leverage of a company by evaluating its debt relative to its equity.

Considering the debt-to-equity ratio in industry comparisons allows for a concise evaluation of a company’s financial health and risk profile, aiding in informed decision-making.

By considering the Debt-to-Equity ratio, AT&T can be compared to its top 4 peers, leading to the following observations:

-

When comparing the debt-to-equity ratio, AT&T is in a stronger financial position compared to its top 4 peers.

-

The company has a lower level of debt relative to its equity, indicating a more favorable balance between the two with a lower debt-to-equity ratio of 1.43.

Key Takeaways

The low P/E and P/B ratios suggest that AT&T may be undervalued compared to its peers in the Diversified Telecommunication Services industry. However, the high P/S ratio indicates that the market values AT&T’s revenue more highly. On the other hand, the high ROE, EBITDA, and gross profit margins suggest that AT&T is efficiently generating profits and cash flow. The low revenue growth rate may be a concern for AT&T’s future performance compared to its industry peers.

This article was generated by Benzinga’s automated content engine and reviewed by an editor.

Recent Comments