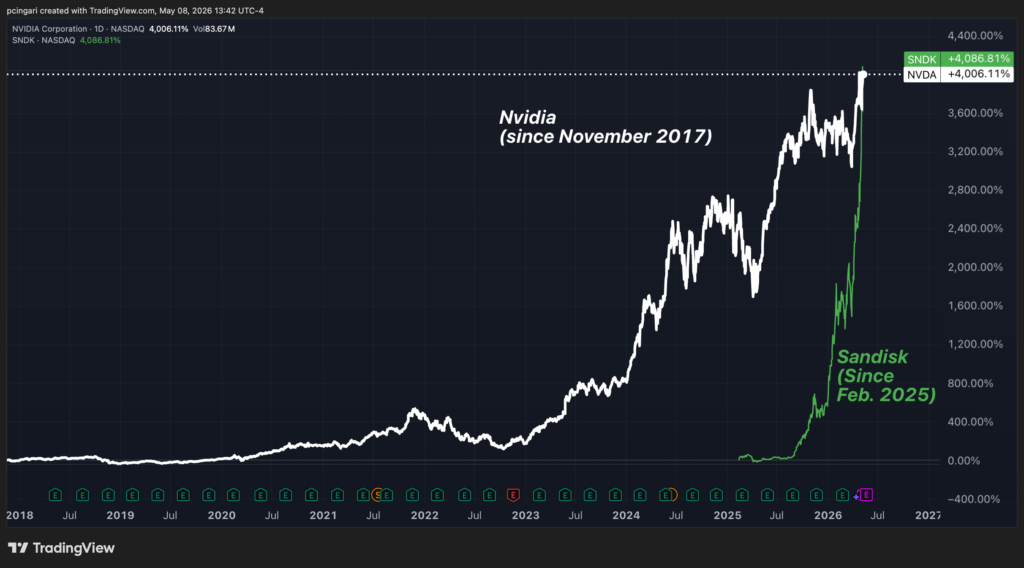

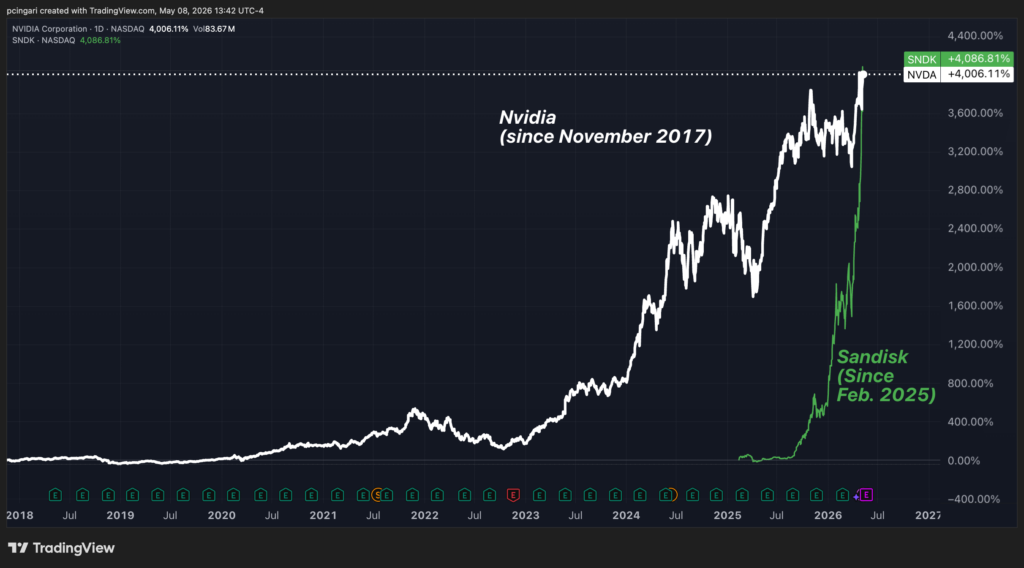

The chart below looks like AI-generated, but it’s not.

Since its February 2025 spin-off from Western Digital Corp. (NASDAQ:WDC), SanDisk Corp. (NASDAQ:SNDK) has gained 4,086%. Nvidia Corp. (NASDAQ:NVDA), the AI poster child of the decade, has gained 4,006% — over nearly nine years.

SanDisk did in 15 months what Nvidia took nearly a decade to deliver.

The reflex on Wall Street has been to call it a meme.

It isn’t.

Behind the parabola sits the most violent supply-demand mismatch the memory industry has seen since 2017, what Wall Street analysts now call the AI memory supercycle.

Nvidia vs. Sandisk Performance Comparison: This Chart Is Shocking Every Trader

The Three Memories That Run AI

Every AI server runs on three different kinds of memory chip, made by largely the same handful of companies.

- DRAM is the working memory. It is what holds the data your computer is actively using — and what holds the parameters of an AI model while it runs. It is fast, but it forgets everything when the power is cut.

- NAND flash is the storage memory. It is what’s inside an SSD or a USB stick. It is slower than DRAM, but it keeps data forever and costs a fraction per gigabyte. AI training datasets, model checkpoints, and retrieval databases all live on NAND.

- HBM, or high-bandwidth memory, is a special kind of DRAM. Engineers stack 8, 12, or 16 DRAM chips on top of each other and bond the stack directly next to a GPU. The result is a memory pipe wide enough to feed an Nvidia GPU at full speed. Without HBM, AI accelerators starve.

Who Makes The Memory Nvidia Buys

The supplier list is short.

Three companies make almost all the world’s DRAM and HBM: Samsung Electronics Co., Ltd. and SK Hynix Inc. of South Korea, and Micron Technology Inc. (NASDAQ:MU) of Idaho.

Together they control more than 95% of global DRAM production and 100% of HBM.

SK Hynix is the king of the hill. It supplies roughly 90% of Nvidia’s HBM. Every Blackwell GPU shipped today carries SK Hynix memory.

For NAND flash, the cast widens by two. Samsung, SK Hynix, and Micron compete with Kioxia Holdings Corp. of Japan and SanDisk.

According to TrendForce, NAND market share at the end of third-quarter 2025 broke down roughly as: Samsung 32%, SK Hynix 19%, Kioxia 15%, Micron 13%, SanDisk 12%. The five together control more than 90%.

That is the entire supplier base for the AI economy. Five companies on three continents.

Why Supply Has Run Out

The bottleneck is mechanical, not narrative.

HBM consumes roughly three times the wafer capacity per gigabyte as standard DRAM, but it sells for ten times the price.

Every Samsung, SK Hynix, and Micron fab on earth has spent the last 18 months converting DRAM lines to HBM as fast as physics allows. According to IDC, up to 70% of all memory chips made globally in 2026 will go to AI data centers.

The result is that everything is short at once. HBM is short because every fab is racing to make it.

Standard DRAM is short because the fabs no longer have room. NAND is short because the same companies make NAND too — and because hyperscalers building AI data centers need vast NAND-based SSDs to store their training data.

Every company involved is now sold out. SK Hynix told investors on its October earnings call that HBM, DRAM, and NAND for 2026 are essentially booked.

Samsung’s memory chief warned on April 30 that significant shortages will continue through at least 2027. SanDisk has gone further — customer conversations now point to tightness extending into 2028.

Hyperscalers are signing three-, five-, and seven-year prepayment contracts to lock in supply. The buyers are absorbing the volume risk this time, not the sellers.

Why SanDisk Is Catching Up Fast

If the squeeze explains why all five names are running, it doesn’t explain why SanDisk has run hardest.

Three reasons.

It’s the only pure-play left. Samsung is a vast conglomerate. SK Hynix and Micron split capacity between HBM, DRAM, and NAND. SanDisk, since its February 2025 spin-off, makes nothing but NAND flash. Investors looking for clean exposure to the storage half of the AI build-out have nowhere else to go.

It made the right capacity bet. Through the painful 2022–2023 memory downturn, SanDisk and its joint-venture partner Kioxia kept production lean. They entered 2026 with a lower cost base than peers. When NAND contract prices surged this year, the bulk of the price increase dropped straight to gross margin. SanDisk’s reported margins are now modeled at 80%-plus through fiscal 2027.

It is leading the next architecture. SanDisk is developing High-Bandwidth Flash, or HBF — the same vertical-stacking idea as HBM, but using NAND instead of DRAM. The pitch: HBM is fast but capacity-limited (Nvidia’s flagship Blackwell GPU carries just 192 GB of it). HBF promises 8 to 16 times the capacity in the same footprint, at lower cost. First samples are expected in the second half of 2026. If HBF becomes the standard, SanDisk’s addressable market roughly doubles.

The numbers back the story. SanDisk reported fiscal third-quarter 2026 revenue of $5.95 billion, up 251% year over year, with datacenter revenue alone jumping 645%.

Why Are Micron And Sandisk Still ‘Cheap’?

Here is where the story turns strange.

The hardware that runs the AI economy — sold out, on multi-year contracts, with 80%-plus margins — is being priced by the market like a cyclical commodity industry staring at a downturn.

| Company | YTD % | (Next 12m) P/E |

|---|---|---|

| SanDisk Corp. | +533% | 9.5x |

| Micron Technology Inc. | +157% | 8.0x |

| Samsung Electronics Co., Ltd. | +126% | 5.3x |

| SK Hynix Inc. | +154% | 5.1x |

| Kioxia Holdings Corp. | +316% | 8.8x |

For comparison: the SPDR S&P 500 ETF Trust (NYSE:SPY) trades at 21.5 times forward earnings. Nvidia trades at roughly 37x.

The world’s most irreplaceable chip companies trade like commodity steel mills.

The reason is simple: earnings are exploding faster than share prices. Micron posted fiscal second-quarter 2026 revenue of $23.86 billion versus $8.05 billion a year earlier, with non-GAAP EPS up 682%.

Goldman Sachs noted Micron alone now accounts for 51% of all S&P 500 EPS revisions this year.

The Street is racing to update models, and the stocks are racing the Street.

What Wall Street Is Saying

Per Benzinga’s Analyst Stock Ratings page, the most recent calls on SanDisk run aggressively above prior consensus.

Bernstein raised its SanDisk target to $1,700 from $1,250 on May 4, reiterating Outperform after a Q3 earnings beat the firm called broad-based with conservative Q4 guidance.

Bank of America, through Wamsi Mohan, lifted its target to $1,550 from $1,080 on May 6, citing strong demand from hyperscalers and the protective effect of new multi-year contracts. The Street-high is $2,000, set by Susquehanna.

The Question The Tape Is Asking

The bear case is not gone. Memory has crashed before. New fab capacity will eventually arrive. A recession or a hyperscaler capex pause could break the contract architecture.

What is unusual about this cycle is how much of that risk has been transferred. Customers are paying upfront, on multi-year contracts. Supply cannot move for years. And the multiples have compressed in the wrong direction — earnings have outrun the stocks.

If SK Hynix at 5x, Samsung at 5x, and Micron at 8x reflect a scenario the operating data refuses to validate, then the rally that took SanDisk past Nvidia in 15 months may not be a peak. It may be a re-rating that hasn’t finished.

Image: Shutterstock

Recent Comments