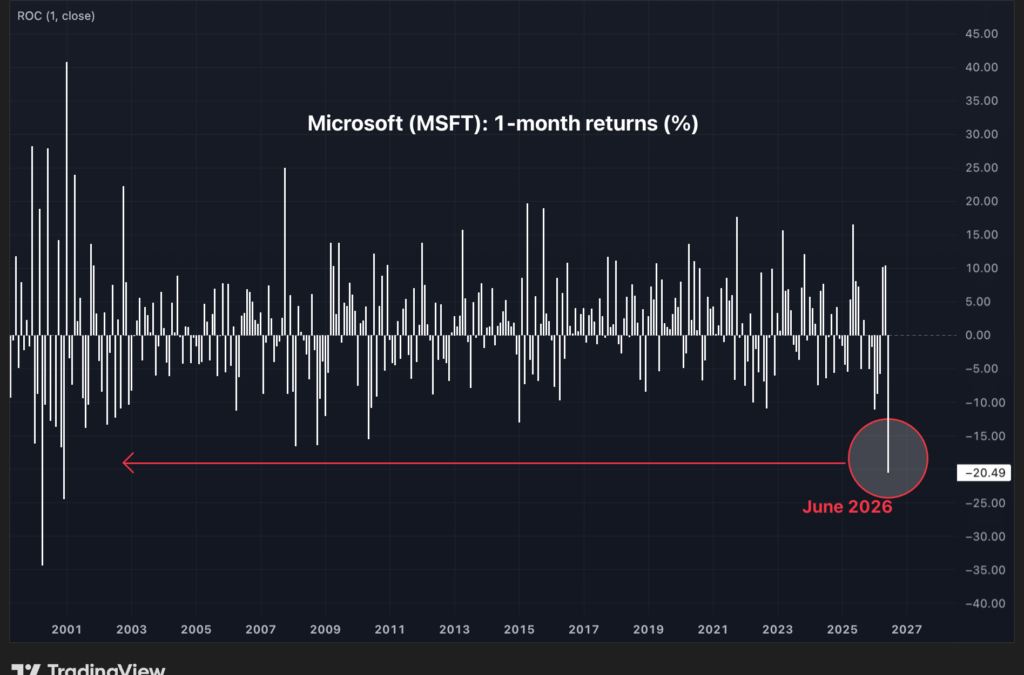

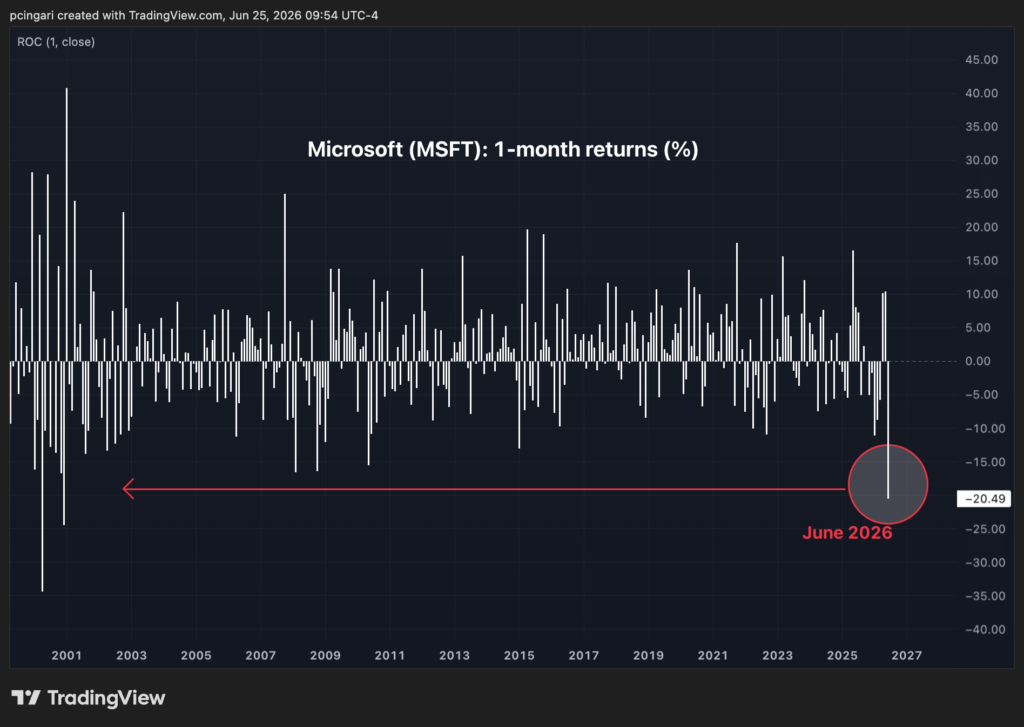

Shares of Microsoft Corp. (NASDAQ:MSFT) are down over 20% in June, on pace for the steepest monthly drop since December 2000.

Twelve months ago, the Redmond, Washington-based company’s market cap hovered around $4 trillion. Today, it’s at $2.65 trillion, behind Nvidia Corp. (NASDAQ:NVDA), Apple Inc. (NASDAQ:AAPL) and Alphabet Inc. (NASDAQ:GOOG).

Yet the business is thriving.

Revenue has grown between 16% and 18% year over year for eight consecutive quarters. Earnings have topped Wall Street estimates every single time and have also been on the rise.

So why is the stock down more than 35% since the start of 2026?

The answer is one word: capex.

Why The Market Stopped Caring What Microsoft Earns Today

Capex — capital expenditure — is the money a company spends on physical infrastructure.

For Microsoft, that means data centers for artificial intelligence. That line of spending, not revenue, is now driving the stock.

Capital spending hit $38 billion last quarter. Bank of America estimates Microsoft’s 2026 capex will approach $190 billion in 2026.

Microsoft is not alone. The five largest hyperscalers — Amazon.com Inc. (NASDAQ:AMZN), Microsoft, Alphabet, Meta Platforms Inc. (NASDAQ:META) and Oracle Corp. (NYSE:ORCL) — are projected to spend over $700 billion in 2026.

The buildout feeds itself. More data centers strain chip and memory supply.

Prices rise. Spending climbs again.

The Chain That Turns Microsoft Into A Falling Stock

Capex up means margins under pressure, which means free cash flow down. Microsoft’s capital spending rose 63% year over year. Free cash flow fell 10%.

Less free cash means fewer buybacks and smaller dividends — the two things that reward shareholders.

Bank of America frames it starkly. Hyperscaler capex has climbed from 70% of operating cash flow in 2025 to nearly 100% in 2026.

Translation: almost no free dollars left for shareholders.

There is another side to the trade. Since January, the semiconductor sector — as tracked by the iShares Semiconductor ETF (NASDAQ:SOXX) — has surged 94%. The Magnificent Seven, tracked by the Roundhill Magnificent Seven ETF (BATS:MAGS), are down about 6%.

Jeff Bezos once said, “Your margin is my opportunity.”

In 2026, that idea has taken on a new meaning.

Every billion that hyperscalers divert away from their own margins is flowing to the companies building the AI stack: memory, semiconductors, cooling systems, optical networking, batteries, power infrastructure, everything required to build AI data centers and train increasingly powerful models.

The market is no longer valuing Microsoft for what it earns today. It’s valuing the enormous cost of what it must build tomorrow.

Is Microsoft investing in the future or sacrificing the present to get there?

Right now, investors seem to believe it’s the latter.

Image: Shutterstock

Recent Comments