An index of commodities excluding energy has just soared to a fresh record high, surpassing the prior peak set in 2011 and signaling that the raw materials rally extends far beyond the crude oil disruption at the Strait of Hormuz.

The Bloomberg Commodity Index ex-Energy topped 155 levels this week, breaking out above its 2011 high and sitting roughly 13% above its 40-week moving average.

The index tracks industrial metals, precious metals, and the agricultural sector — everything that ends up inside a power cable, a solar panel, a data center cooling loop, or a fertilizer bag.

It is a record set without crude oil. The move is structural. And it is wired directly into the AI race.

“While energy markets have captured most of the attention since the start of the Iran conflict, strength across the broader commodity complex has been equally notable this year,” said Adam Turnquist, chief technical strategist for LPL Financial, in an emailed note.

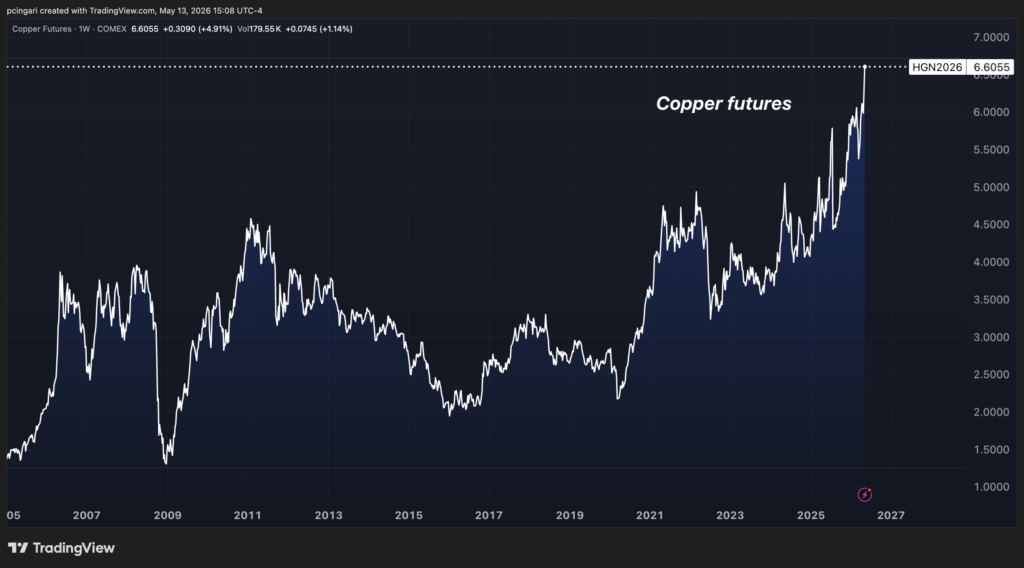

Copper Is The Tell

Turnquist flagged the breakout in a research note on Tuesday and linked it to a list of drivers that bear little resemblance to the 2011 emerging-market reflation trade.

Tight supply. Chinese silver export restrictions. Solar. AI data centers. Electric vehicles. Lithium carbonate has more than doubled this year due to accelerating demand for batteries and energy storage.

Copper has climbed to record highs on what Turnquist called “rising consumption tied to AI data center buildouts and electrification trends.”

Copper futures on COMEX — as closely tracked by the United States Copper Index Fund ETV (NYSE:CPER) — traded above $6.64 a pound on Wednesday, a fresh all-time high.

London Metal Exchange copper hit $14,196.50 per ton, within touching distance of its $14,527.50 record.

The metal is up roughly 16% year-to-date and 43% year-over-year, sitting on its eighth straight day of gains.

The supply shock is real. The Hormuz closure has fractured the seaborne sulfuric acid trade. Turns out, sulfuric acid is what copper miners use in heap leaching to extract metal from ore.

The Middle East supplies nearly half the world’s seaborne sulfuric acid market.

Chilean copper production already fell by roughly 6% in the first quarter of 2026 compared with the prior year. China has banned sulfuric acid exports through at least December.

Freeport–McMoRan Inc. (NYSE:FCX)‘s Grasberg, the world’s second-largest copper mine, is still operating below full capacity following last September’s landslide. The company does not expect it to be back at full tilt until late 2027.

But the demand side is where the AI story lives.

A ‘New Era’ For Copper

Kathleen Quirk, president and CEO of Freeport-McMoRan Inc., spoke at Bank of America’s Global Metals, Mining & Steel conference in Miami this week and described copper as now in a “new era” tied to electricity demand — electrification, AI data centers, and grid investment.

Quirk said Freeport acquired Phelps-Dodge in 2007 and has been positive on copper ever since, originally betting on China urbanization.

What changed is the demand pile-up.

“FCX sees itself as well-positioned both in terms of current production and the greenfield pipeline,” according to Bank of America analyst Jason Fairclough.

Freeport is not alone. Citi strategists wrote in a note Monday that “practically all copper demand growth since 2022 has come from energy transition and AI related sources.”

The math behind the AI demand line is unsubtle. An AI data center consumes up to three times more copper than a traditional data center, with hyperscale facilities pulling as much as 50,000 tons each.

OpenAI Inc.‘s $500 billion Stargate initiative, along with capex commitments from Microsoft Corp (NASDAQ:MSFT), Alphabet Inc (NASDAQ:GOOGL), Meta Platforms Inc (NASDAQ:META), and Amazon.com Inc (NASDAQ:AMZN), all hit the same constraint: every gigawatt of new compute needs busbars, switchgear, transformers, and cabling.

By 2030, AI-related copper consumption could exceed 500,000 metric tons annually, nearly 2% of current global mine output.

Mine supply growth for 2026 is estimated at 1.4%.

Silver Is Running Even Harder

Silver – as closely tracked by the iShares Silver Trust (NYSE:SLV) – is up 166% year-over-year and 23% year-to-date, trading near $87.85 an ounce.

The driver is not Fed-cut speculation. It is industrial demand.

Roughly 60% of silver consumption is now industrial. Solar photovoltaic panels alone are projected to absorb 120 to 125 million ounces of silver in 2026.

AI hardware, electric vehicles, power electronics, and high-density data center components are adding to the load.

The Silver Institute is projecting a 67 million-ounce supply shortfall this year, the fifth consecutive deficit.

Tight Chinese export restrictions announced earlier this year have made the squeeze worse.

Platinum is up 119% year-over-year. Lithium carbonate is up 189%. Cobalt hydroxide is up 88%. These are not safe-haven trades.

They are bottleneck trades on the materials that get poured into the semiconductor supply chain, the grid, and battery storage that backs up AI compute farms.

What This Means For Investors

The macro chain reads cleanly: AI capex is accelerating.

AI capex requires unprecedented quantities of copper, silver, aluminum, and rare earths. Supply is constrained by Hormuz, by structural underinvestment, by Chinese export curbs, and by depleting ore grades.

Prices rise. Input costs across manufacturing, construction, transportation, and food production move with them.

Turnquist warned that if the breakout holds, “rising prices across industrial metals, precious metals, and agricultural commodities — not just oil — could create broader inflationary pressures by lifting input costs across manufacturing, construction, transportation, and food production. That dynamic could make it more difficult for inflation to moderate in the months ahead, even if energy prices eventually stabilize.”

U.S. producer prices rose 1.4% in April, the largest monthly gain since March 2022, with the headline index up 6.0% year-over-year, the highest since December 2022.

If AI is the new electricity, then copper is the new oil. Silver is the new conductor. Lithium is the new gasoline.

And the companies racing to build out the physical layer of the AI economy — Nvidia Corp. (NASDAQ:NVDA), the hyperscalers, the chip fabs, the utilities — are all bidding for the same finite pile of raw materials.

Image: Shutterstock

Recent Comments