This week, the Bank of Japan wrecked havoc on the foreign exchange market. What’s the Yen Carry Trade, how does an intervention work, and what does it all mean?

Yen Carry Trade – A Massive Money Printer

Years ago, a massive money printer emerged out of Japan. It was called “The Yen Carry Trade”, and it provided trillions of dollars of capital that would flow into US Treasuries, stocks, and other financial assets.

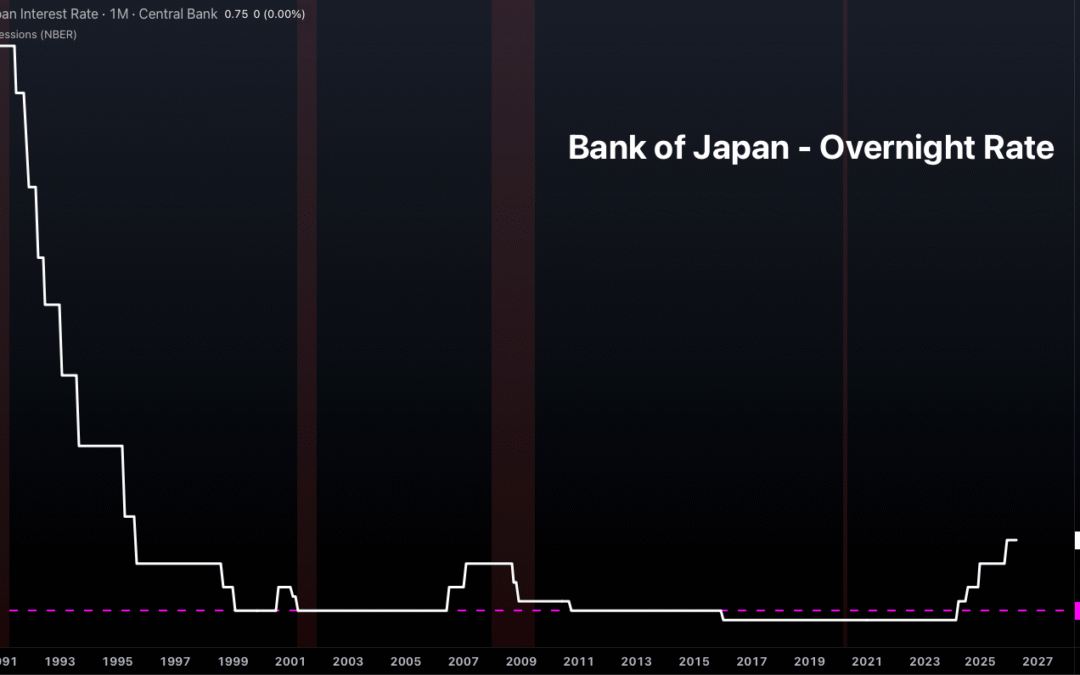

To deal with the enormous economic pain that Japan was suffering after the 1990 bubble burst, the Bank of Japan took its overnight interest rate to 0.0%, and from 2016-2024, even negative.

Japanese overnight interest rate, 1990-present

Remember, the central bank’s overnight interest rate is the price of money. In this case, they made the Yen not just free, but for a brief period, they were paying you to take out Yen loans.

It worked.

Trillions of dollars worth of Yen-denominated loans were taken out. But due to the historically easy monetary policy of ZIRP/NIRP, people didn’t want to hold onto a currency whose value was being crushed. Therefore, people immediately sold the Yen they had just gotten and bought dollars.

Overnight rate versus JPY/USD exchange rate

This selling pressure, coupled with poor economic growth and easy monetary policy, led to an immense amount of weakness for the Yen. In the past 15 years, the Yen has lost 49% of its value versus the dollar.

Taking out Yen loans at 0%, buying dollars and just waiting for the currency to weaken (which already would have yielded a positive return), was not enough-

Investors took out JPY at 0%, sold the Yen/bought dollars, then put those dollars into positive yielding instruments like US Treasuries, Mortgage Backed Securities, and even stocks. Not only were they making money from the dollar strengthening (meaning over time, fewer dollars would be required to pay their Yen loan back), but they also had a positive return from the dollar investment into bonds, stocks, etc.

What could go wrong?

The Problem

There was one small problem- the Yen couldn’t be allowed to weaken too much, or else Japan would suffer from the problem of domestic inflation given their reliance on food and energy imports.

This wasn’t too much of a concern for much of the last two decades (as GDP, inflation and wages were occasionally even negative), but in 2022 everything started to change-

Economic growth, including inflation, started to actually accelerate.

Overnight rate, versus domestic inflation rate (not prolonged periods of deflation).

This led to a huge problem for policymakers – they couldn’t allow inflation to get too far out of hand, or they’d risk losing complete control over their currency as well as suffering from political consequences from high inflation.

Therefore, they started to hike interest rates, albeit from a very low starting point. The first hike occurred in the spring of 2024, then, of course, everything imploded with the subsequent hike in the summer of 2024, leading to some major issues in the US financial system.

Nasdaq would decline 14% and the VIX (fear gauge) would soar to 40.

Nasdaq, Dollar/Yen and JP Overnight rate – the 2024 “Yen Carry Trade Unwind”

It was a short squeeze. Everyone who had borrowed Yen, then converted it to dollars, was by definition short the Yen.

And the Yen was absolutely soaring…

Currency Intervention – Major Consequences

One of the reasons that the developments in the oil market are so incredibly important is that the higher price of oil puts a massive strain on economies like Japan that are net importers of energy (about 90%).

Not only is oil soaring in dollar terms (which is the way the majority of oil transactions are priced), but it’s rising even more in Yen terms.

Dollar/Yen exchange rate, versus Crude oil prices since the start of the war

This is where we found ourselves this past week- oil was soaring and therefore, global bond yields were ripping higher (on higher inflation fears) and net importers were facing major weakness in their currencies.

This is where the Japanese government decided to engage in currency manipulation, or more politely put, “currency intervention”.

In an intervention, the Bank of Japan is instructed by the Japanese Finance Ministry on the details, such as size, and then the Bank of Japan dumps its liquid dollar holdings to buy Yen. Most of these USD holdings are in liquid instruments like T-bills (short-duration Treasuries) that can be liquidated with minimal consequences.

The dollars from those sales are then immediately dumped and used to buy Yen.

This causes some absolutely insane moves in the currency market- over approximately four hours, the dollar would lose 3% of its value (vs the Yen), as the Bank of Japan ruthlessly dumped dollars to buy Yen. Another smaller intervention may have occurred shortly thereafter.

Dollar/Yen exchange rate through the intervention

Remember, the Yen Carry Trade means that you’re short the Yen because you eventually need to pay your loan back in Yen. In other words, you’re long USD/JPY, and you just had a HUGE seller start dumping on your position.

These carry trades are usually leveraged, so even a 5-10% move could prove very troubling (as we saw in summer of 2024). If you get a margin call, the order of operations would be reversed from putting the trade on:

Sell: Treasuries, Stocks, etc ➡️ Sell: Dollars ➡️ Buy: Yen ➡️ Cover Yen loan/close

One important note that is missed in the vast majority of discourse on Japan, the Yen, Bank of Japan:

Just as levered hedge funds put on a positive carry trade, so too did the Japanese government. By issuing domestic JGB debt at 0% and buying US Treasuries at 2-5% (Japan is the largest sovereign holder of debt at over $1.2 trillion), the Japanese government is making record net interest income.

The Yen Carry Trade is making them about $50 billion a year in net interest income- enough to fund their entire fiscal deficit for 3 years.

Not only that, but the weakness in their currency has led to staggering unrealized gains on their USD-denominated treasury holdings.

So far, we have not suffered the same consequences this time around, but further intervention could very well bring more liquidation of assets that were purchased via the Yen Carry Trade (including, possibly, BTC).

With the Bank of Japan on an interest rate hiking cycle, and these fx interventions becoming more and more commonplace, one of the large incremental drivers of global liquidity is vanishing into thin air.

With all of the unpredictable policies of elected leaders, bitcoin’s hard-coded monetary policy emerges as quite the breath of fresh air…

WANT MORE WOLF? Follow us on YouTube

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.

Recent Comments