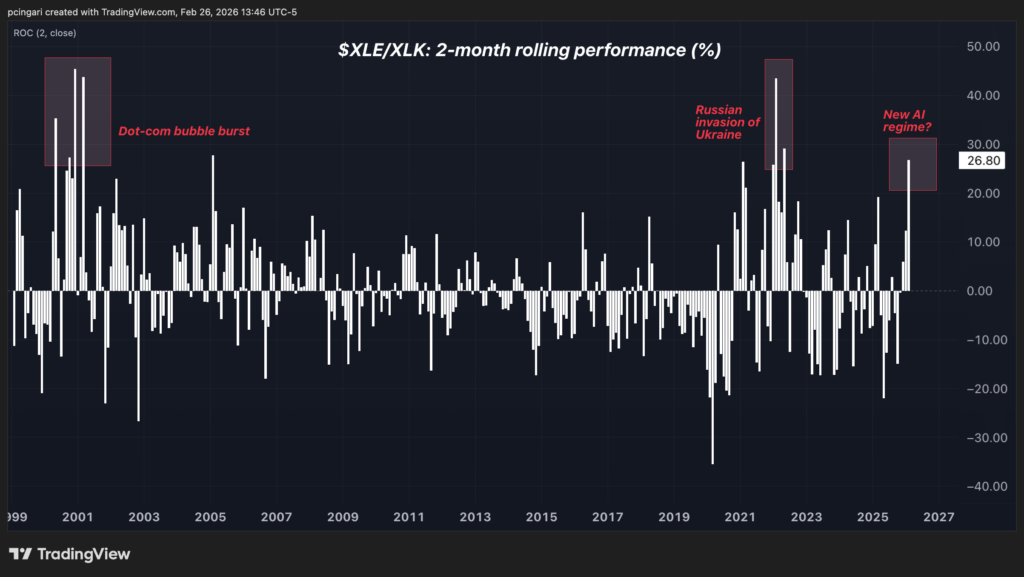

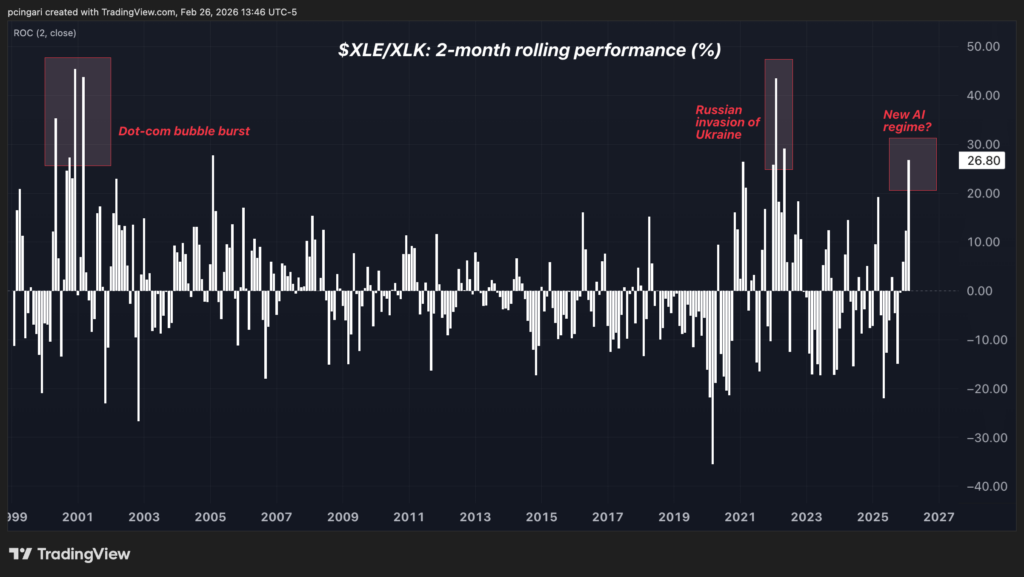

The first two months of 2026 have produced a sector divergence not seen on Wall Street since the shock of February 2022.

Back then, Russia’s invasion of Ukraine triggered a violent rotation into energy and commodities.

Oil spiked. Defense stocks surged. Technology sold off on inflationary concerns.

Now it’s happening again — but for a very different reason.

Through Feb. 26, 2026, the Energy Select Sector SPDR Fund (NYSE:XLE) has outperformed the Technology Select Sector SPDR Fund (NYSE:XLK) by 27 percentage points.

That is the largest two-month performance gap between Energy and Technology since February 2022.

The contrast becomes even more dramatic when you line up the VanEck Oil Services ETF (NYSE:OIH) against the iShares Expanded Tech-Software Sector ETF (NYSE:IGV): over just two months, the performance gap has blown out to a staggering 80 percentage points.

Unlike four years ago, there has been no oil supply shock, no sudden war escalation and no surge in crude comparable to the post-invasion spike.

Instead, the growing gap between energy and tech reflects a new shift — one driven by AI.

Wall Street Is Rotating — Not Retreating

Crucially, investors are not abandoning equities.

They are reallocating within them.

Energy, materials and industrial stocks have led gains since the start of the year. Technology, communication services and financial are lagging.

Equal-weight indices have recently outperformed capitalization-weighted benchmarks — often interpreted as a sign that returns are spreading beyond a handful of mega-cap technology names.

The Invesco Equal-Weight S&P 500 Index (NYSE:RSP) has outperformed the cap-weighted SPDR S&P 500 ETF Trust (NYSE:SPY) by 5 percentage points year-to-date.

Notably, the Invesco S&P 500 Equal Weight ETF has outperformed the SPDR S&P 500 ETF Trust for four consecutive months — the longest such stretch since January 2023.

The AI paradox

Artificial intelligence was supposed to lift the whole technology sector. Instead, it is redrawing the map.

AI increases productivity, but it can also squeeze margins in labour-intensive businesses.

If software, coding or customer support can be automated at near-zero cost, investors inevitably question how durable those profits really are.

At the same time, the companies building AI are spending heavily on data centers, power supply and industrial equipment.

AI may be digital, but it runs on concrete, steel and electricity.

The HALO Trade And The Map Of The New AI Winners

A new analysis from Goldman Sachs suggests investors are beginning to price in which industries benefit from AI — and which are vulnerable to it.

The firm screened companies based on two factors: how exposed their labor force is to AI-driven automation, and how large labor costs are relative to revenue.

Sectors such as software, professional services and media rank high on both measures — meaning their margins could face structural pressure if AI reduces the scarcity of white-collar work.

By contrast, energy, utilities, materials and other asset-heavy industries carry lower labor intensity and higher tangible asset backing.

Goldman calls the emerging leadership theme HALO — Heavy Assets, Low Obsolescence.

In other words, the market may be shifting its premium from scalable code to hard-to-replicate infrastructure.

If that framework holds, the widening gap between energy and technology isn’t just a trade.

It’s the consequence of investors repricing what scarcity looks like in an AI-driven economy.

Image created using artificial intelligence via Midjourney.

Recent Comments