Editor’s note: The article was corrected to remove references to incorrect currency translation in foreign competitors.

Amidst the fast-paced and highly competitive business environment of today, conducting comprehensive company analysis is essential for investors and industry enthusiasts. In this article, we will delve into an extensive industry comparison, evaluating Tesla (NASDAQ:TSLA) in comparison to its major competitors within the Automobiles industry. By analyzing critical financial metrics, market position, and growth potential, our objective is to provide valuable insights for investors and offer a deeper understanding of company’s performance in the industry.

Tesla Background

Tesla is a vertically integrated battery electric vehicle automaker and developer of real world artificial intelligence software, which includes autonomous driving and humanoid robots. The company has multiple vehicles in its fleet, which include luxury and midsize sedans, crossover SUVs, a light truck, and a semi truck. Tesla also plans to begin selling a sports car and offer a robotaxi service. Global deliveries in 2024 were a little below 1.8 million vehicles. The company sells batteries for stationary storage for residential and commercial properties including utilities and solar panels and solar roofs for energy generation. Tesla also owns a fast-charging network and an auto insurance business.

| Company | P/E | P/B | P/S | ROE | EBITDA (in billions) | Gross Profit (in billions) | Revenue Growth |

|---|---|---|---|---|---|---|---|

| Tesla Inc | 308.41 | 18.60 | 16.48 | 1.75% | $3.66 | $5.05 | 11.57% |

| General Motors Co | 15.89 | 1.17 | 0.45 | 1.95% | $5.74 | $3.11 | -0.34% |

| Ferrari NV | 34.41 | 14.50 | 7.79 | 10.42% | $0.67 | $0.88 | 7.4% |

| Ford Motor Co | 11.95 | 1.18 | 0.30 | 5.29% | $3.67 | $4.3 | 9.39% |

| Li Auto Inc | 15.23 | 1.62 | 0.86 | -0.86% | $-0.71 | $4.47 | -36.17% |

| Thor Industries Inc | 21.89 | 1.42 | 0.63 | 0.5% | $0.11 | $0.32 | 11.5% |

| Winnebago Industries Inc | 35.99 | 1.05 | 0.45 | 0.45% | $0.03 | $0.09 | 12.32% |

| Workhorse Group Inc | 0.07 | 1.47 | 0.35 | -28.77% | $-0.01 | $-0.01 | -4.97% |

| Average | 18.21 | 2.96 | 1.47 | -1.06% | $229.23 | $247.75 | 0.91% |

By thoroughly analyzing Tesla, we can discern the following trends:

-

The current Price to Earnings ratio of 308.41 is 16.94x higher than the industry average, indicating the stock is priced at a premium level according to the market sentiment.

-

With a Price to Book ratio of 18.6, which is 6.28x the industry average, Tesla might be considered overvalued in terms of its book value, as it is trading at a higher multiple compared to its industry peers.

-

With a relatively high Price to Sales ratio of 16.48, which is 11.21x the industry average, the stock might be considered overvalued based on sales performance.

-

The company has a higher Return on Equity (ROE) of 1.75%, which is 2.81% above the industry average. This suggests efficient use of equity to generate profits and demonstrates profitability and growth potential.

-

With lower Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) of $3.66 Billion, which is 0.02x below the industry average, the company may face lower profitability or financial challenges.

-

With lower gross profit of $5.05 Billion, which indicates 0.02x below the industry average, the company may experience lower revenue after accounting for production costs.

-

The company’s revenue growth of 11.57% exceeds the industry average of 0.91%, indicating strong sales performance and market outperformance.

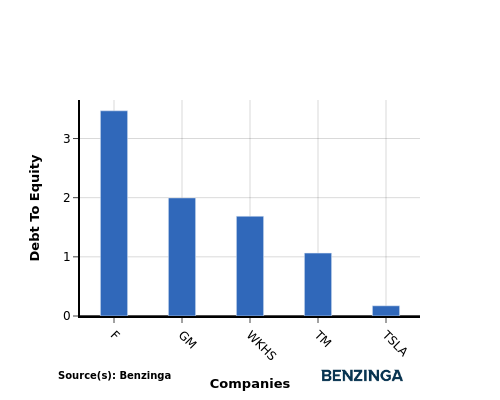

Debt To Equity Ratio

The debt-to-equity (D/E) ratio measures the financial leverage of a company by evaluating its debt relative to its equity.

Considering the debt-to-equity ratio in industry comparisons allows for a concise evaluation of a company’s financial health and risk profile, aiding in informed decision-making.

When examining Tesla in comparison to its top 4 peers with respect to the Debt-to-Equity ratio, the following information becomes apparent:

-

In terms of the debt-to-equity ratio, Tesla has a lower level of debt compared to its top 4 peers, indicating a stronger financial position.

-

This implies that the company relies less on debt financing and has a more favorable balance between debt and equity with a lower debt-to-equity ratio of 0.17.

Key Takeaways

The high PE, PB, and PS ratios suggest that Tesla is relatively overvalued compared to its peers in the Automobiles industry. On the other hand, the high ROE and revenue growth indicate strong profitability and potential for future growth. However, the low EBITDA and gross profit figures may raise concerns about Tesla’s operational efficiency and financial health within the industry sector.

This article was generated by Benzinga’s automated content engine and reviewed by an editor.

Recent Comments