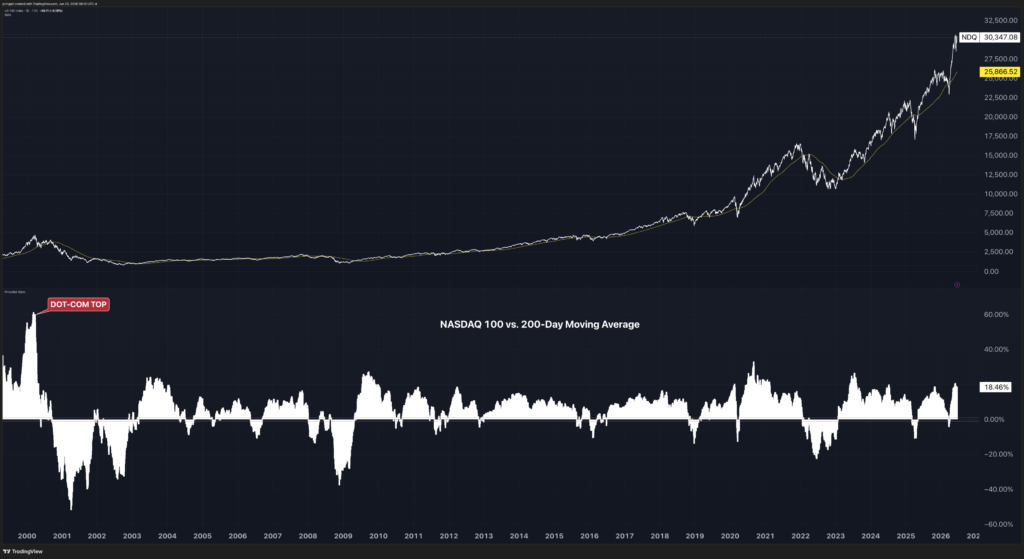

The Nasdaq 100 is back near record territory, trading around 30,350, and it sits roughly 18% above its 200-day moving average.

That looks stretched until you set it against the last time anyone called technology stocks a bubble.

At the peak of the dot-com mania in early 2000, the index ran nearly 60% above the same trend line. Today’s premium is barely a third of that.

The distance between price and the 200-day moving average is one of the bluntest measures of how far a market has sprinted ahead of its own trend. The wider it stretches, the more a rally relies on momentum rather than fundamentals.

By that yardstick, the current advance looks contained. The tech-heavy index – as tracked by the Invesco QQQ Trust (NASDAQ:QQQ) – stands about 18.5% above its long-term average, well inside a band it has revisited repeatedly over twenty years without a major selloff following.

Chart: Nasdaq 100 vs. 200-Day Moving Average

FOMO Built The Last Bubble, FEMO Is Driving This Rally

Market veteran Ed Yardeni indicated this week that the character of the rally matters more than its altitude.

Yardeni said the current rally is increasingly being driven by what he calls FEMO, or “Fabulous Earnings Momentum,” rather than FOMO, the fear of missing out that characterized the dot-com era.

“The stock market bubble of the late 1990s was driven by FOMO on the tech-led bull market,” Yardeni wrote. At the time, the forward price-to-earnings ratio of the S&P 500 climbed to 25, while the technology sector’s forward multiple surged to an extraordinary 55.

Today, the picture looks markedly different.

The S&P 500 trades at roughly 20.4 times forward earnings, while the Information Technology sector commands a forward P/E of about 23. Those figures are elevated relative to historical norms but nowhere near the extremes seen a quarter-century ago.

“An earnings-led rally should be much more sustainable than a P/E-led one fueled by irrational exuberance,” Yardeni said. “FEMO beats FOMO.”

The Earnings Are There, Euphoria Is Not

The earnings story has hard numbers to back it up.

Goldman Sachs estimates S&P 500 first-quarter earnings per share grew about 25% from a year earlier. Strip out the other-income contribution from Amazon.com Inc. (NASDAQ:AMZN) and Alphabet Inc. (NASDAQ:GOOGL) and growth still ran near 16%, with the median stock up about 11%.

For the upcoming quarters and until the fourth quarter of 2027, earnings are expected to grow in double digits.

That distinction matters because corporate profits are growing alongside stock prices rather than merely being justified by expanding valuation multiples.

Critical Difference

During the dot-com boom, stock prices soared despite limited profits and often nonexistent business models.

Today’s leaders — including AI-related semiconductor and software companies — are generating substantial cash flow and delivering earnings growth that is exceeding analyst expectations.

That doesn’t mean risks have disappeared.

Yardeni highlighted growing concerns that AI-related firms may be boosting one another’s results through intertwined capital spending and investment activity, raising questions about the sustainability of current earnings trends.

Still, the strategist sees little evidence that investors have reached the level of irrational exuberance that prevailed in 2000.

For now, the data suggest technology stocks are expensive, but not bubble-like by historical standards.

Image: Shutterstock

Recent Comments