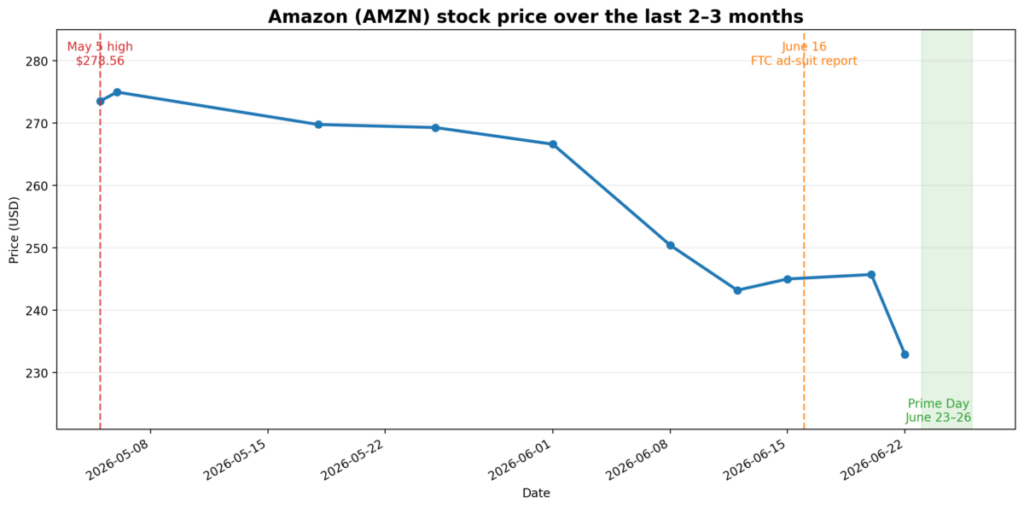

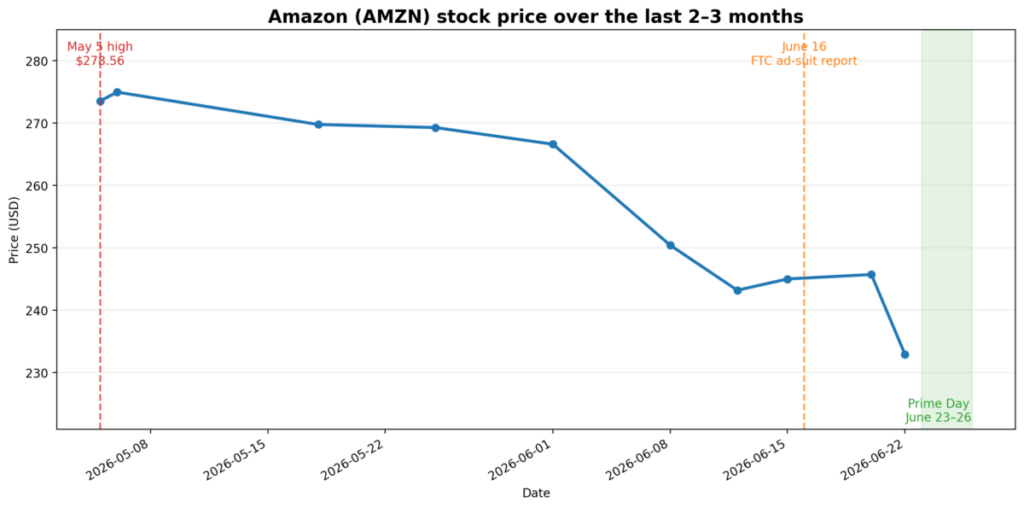

Amazon (NASDAQ:AMZN) shares fell 4.08% on Monday, sliding from a previous close of $244.39. If you have been watching this stock for the past few weeks, the move probably did not shock you. It is just the newest chapter in a slide that started back in May.

Here is the strange part. Amazon’s cloud business just posted its best growth in nearly four years. The company is making more money from operations than it has in a long time. And yet the stock keeps sliding.

The real story is that Amazon is asking investors to believe in three things at once right now: that shoppers will keep spending, that its ad business will dodge a costly legal fight, and that its massive AI spending bill will pay off before patience runs out. When the market gets less sure about any one of those three, the stock takes a hit. That is worth understanding before Prime Day kicks off this week.

The Slide Did Not Start Today

Amazon hit a 52-week high of $278.56 back on May 5. Measured from that high, the stock is now down roughly 16%. So today’s 4% dip is not some one-time gut punch. It is the latest leg of a slide that has been going on for nearly two months.

Think of it like a tire with a slow leak rather than a blowout. No single pothole caused this. Instead, a handful of pressures have been pressing down on the stock at the same time, and today just added a bit more air loss.

So what are those pressures? A Prime Day that Wall Street is treating differently than usual, a fresh legal headache over how Amazon sells ads, and the giant pile of cash the company is pouring into AI. Let’s walk through each one.

Prime Day Just Became a Stress Test

Amazon’s Prime Day usually feels like a victory lap. The company flexes its sales numbers, analysts nod along, and everyone moves on. This year feels different.

Prime Day runs June 23 through June 26, a full month earlier than usual. Reuters is framing the event as something closer to a checkup on the American shopper’s wallet, with early signs pointing toward more spending on groceries and everyday basics rather than splashy discretionary buys like TVs or vacations.

Picture it this way. If your friend tells you they are excited to spend their bonus on a new gaming console, that says one thing about their finances. If they tell you they are excited because the bonus means they can finally restock the pantry without stressing, that tells you something very different. Wall Street is watching which version of that story Prime Day tells this year.

Data tracking firm eMarketer expects Amazon to pull in $15.7 billion in US sales over the four days, a 7% jump from last year. That sounds healthy on paper. But the mix of what people buy may end up mattering more to investors than the total dollar figure.

The FTC Has Questions About How Amazon Sells Ads

Here is the freshest piece of news weighing on the stock, and it is a bit more interesting than the usual “regulators are looking into Amazon” headline.

Bloomberg reported, citing people familiar with the matter, that the Federal Trade Commission has drafted a potential complaint over claims that Amazon misled advertisers. No lawsuit has actually been filed yet, and no charges have been confirmed. This is still a probe, not a verdict. But it is a serious one, and it centers on something called “reserve pricing.” When a business wants to buy an ad on Amazon, it enters into a kind of auction. Reserve pricing is the hidden minimum bid a business has to clear before its ad can even show up. Regulators want to know whether Amazon properly told advertisers that floor existed.

Here is a simple way to picture it. Imagine bidding at an auction house, except the auctioneer never tells you there is a secret reserve price you have to beat. You think you are bidding against other buyers in the room. In reality, you might be bidding against a number only the auction house can see, and you have no way of knowing if your bid was ever competitive in the first place. That is the core question regulators are asking about Amazon’s advertising business, which pulled in roughly $68.6 billion in revenue last year according to a company filing.

The penalty math here is also worth knowing. The FTC’s own power to fine companies is fairly limited by law. But several state attorneys general are reportedly involved in this investigation too, and state consumer protection laws allow for fines that stack up daily, per violation. When you are talking about a platform that serves an enormous number of ads every single day, those daily fines can snowball into billions fairly quickly. Regulators could settle this or move toward a lawsuit as soon as this summer, though nothing is final yet.

Worth noting for context: this would not be Amazon’s first brush with the FTC. The company agreed last September to pay $2.5 billion to settle a separate case over how it signed people up for Prime memberships. That earlier case is closed and is not evidence of wrongdoing in this new one, but it does mean Amazon is heading into a possible third regulatory front in just a few years, alongside an antitrust trial over marketplace pricing that is expected in early 2027.

There is also a timing wrinkle worth flagging for anyone trading around this. Amazon’s next earnings report is tentatively set for July 30. If regulators move toward a lawsuit or settlement before then, that legal headline could land in the same window as quarterly results, which would stack two market-moving events on top of each other. On top of that, the refund deadline for Prime members covered under the earlier $2.5 billion settlement falls on July 27, just three days before earnings. None of this guarantees fireworks, but it does mean late July is shaping up to be a busy stretch for anyone holding this stock.

The AI Spending Bill Keeps Growing

The third pressure point is the one that has been building the longest: how much Amazon is spending to build out AI infrastructure.

Amazon plans to spend roughly $200 billion this year on data centers, custom chips, and other AI related buildout. That is an enormous number, and it has been squeezing free cash flow even as the underlying business keeps growing.

A simple way to think about it: spending heavily today to build something that pays off later always looks worse on paper in the short run than it will look once the investment matures. Operating cash flow, the money coming in from the actual business, jumped 20% over the past year to about $139.5 billion. But free cash flow, what is left after all that AI spending, dropped sharply because so much money went straight into building things. Investors are split on whether this spending will pay off fast enough to justify the price tag, and that disagreement shows up as volatility in the stock.

Why the Stock Looks Cheap Even Though the Business Looks Strong

Put all three pieces together and you get the real puzzle. Amazon Web Services, the cloud computing arm, grew 28% year over year last quarter. That is its fastest growth pace in 15 quarters, with record profit margins to match. Normally, a number like that sends a stock higher, not lower.

Instead, Amazon now trades at a lower multiple of its expected operating profit than it did for most of last year, even with growth accelerating. In plain terms, the market is paying less for each dollar of Amazon’s future earnings than it was paying twelve months ago. That mismatch is the heart of the debate among investors right now. Some see a buying opportunity in a great business going through a rough patch. Others worry the spending will not pay off quickly enough and the stock deserves to trade cheaper until proven otherwise.

A Side Note Worth Watching: Amazon Stays Quiet on Prime Day Numbers

One more thing worth knowing, even if it is not moving the stock today. Amazon has never released hard sales figures for Prime Day. It usually just says some version of “our biggest Prime Day ever” and leaves it there. Meanwhile, competitor Shopify has shared its own holiday sales numbers since 2021, and British retailer John Lewis used to publish weekly sales figures for years.

Given how much weight markets are now putting on guessing Amazon’s numbers, some voices on Wall Street think Amazon should simply share real figures once the event wraps up Friday. Whether or not that happens, the silence itself is part of why every Prime Day turns into a guessing game for analysts and traders alike.

What This Means If You Are Watching the Stock

None of this means Amazon is broken at all. The core business is still growing, AWS just had one of its best quarters in years, and the company still has 63 analysts rating it a buy versus zero sell ratings, with an average price target well above where the stock sits today.

What it does mean is that the stock is being asked to answer three important questions at the same time: Is the American shopper still spending freely or pulling back to basics? Will the ad business face a costly legal setback? And will the AI spending spree start paying off before patience runs out?

Until those answers get clearer, expect more days like today, where good news on one front gets drowned out by uncertainty on another.

Prime Day kicks off Tuesday. Whatever numbers come out of it, even informal ones, will likely become the next data point in this same tug of war.

image credit: Author

This article is for informational purposes only and does not constitute investment advice. Stock prices and figures cited reflect data available as of June 22, 2026, and are subject to change.

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.

Recent Comments