April 2026 will go into the books as one of the most extraordinary months in modern Wall Street history.

The Nasdaq 100 closed the month up 15.6% — its best month since 2002. The S&P 500 added 10.5%, its best since November 2020. The iShares Semiconductor ETF (NASDAQ:SOXX) surged 40%, marking the best monthly performance in the index’s history.

Intel Corporation (NASDAQ:INTC) was the poster child of the rally. Shares ended the month up 119% — the best month in the company’s history, nearly double the previous record set in October 1974.

Elsewhere, Advanced Micro Devices Inc. (NASDAQ:AMD) rose 74% (its best since January 2001), Marvell Technology Inc. (NASDAQ:MRVL) added 66%, Micron Technology Inc. (NASDAQ:MU) gained 53%, Alphabet Inc. (NASDAQ:GOOGL) (NASDAQ:GOOG) climbed 33.8% and Amazon.com Inc. (NASDAQ:AMZN) rose 27.3% — each posting the strongest month in two decades or more.

A wave of mega-cap tech earnings — all beating estimates and raising AI capex guidance — did the heavy lifting.

Then came Wednesday — the most divided Federal Open Market Committee meeting since 1992.

Governor Stephen Miran called for a 25-basis-point cut, while three regional Fed presidents pushed back against the easing bias in the statement.

Chair Jerome Powell confirmed he will hand over the role to Kevin Warsh on May 15, but will remain on the Federal Reserve’s Board of Governors.

Markets read the message clearly: the Fed is uneasy about inflation, divided on its next move, and unwilling to commit to cuts.

Suddenly, the fear of rate hikes is back on the table.

Thursday delivered the receipts. First-quarter GDP came in below expectations at 2%, held up almost entirely by AI-related capex.

But the Fed’s preferred inflation gauge rose to 3.2%, moving further away from the 2% target.

Iran provided the week’s tail risk. Talks stalled throughout the week, Brent crude oil climbed near $120, then on Friday morning, Tehran routed a fresh proposal through Pakistani mediators, calming oil markets.

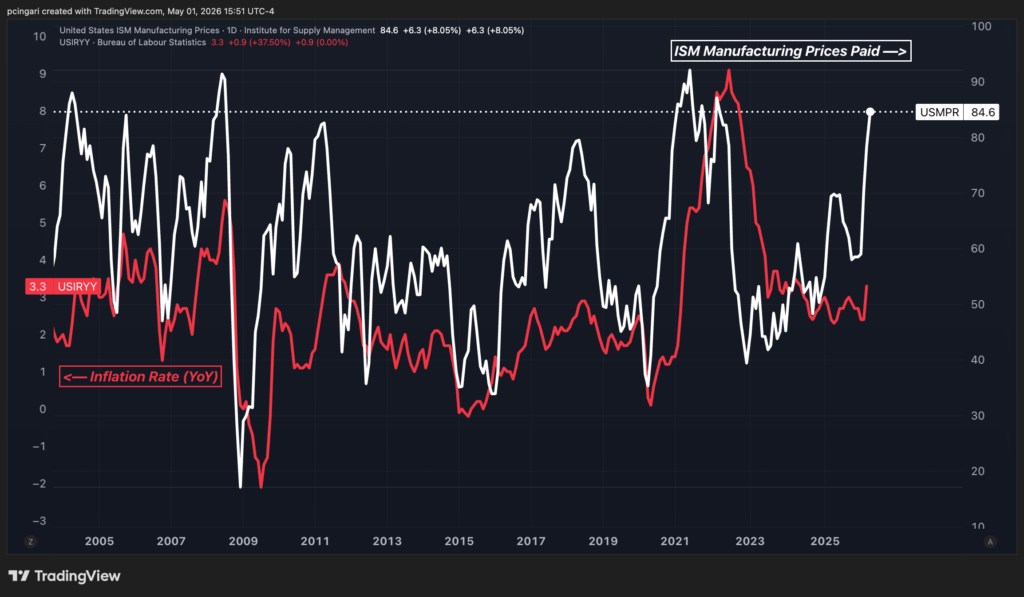

The week’s final word came from the factory floor. The April ISM Manufacturing PMI held at 52.7 — matching its highest level since August 2022 — but the prices-paid component surged at the fastest pace since late 2021, driven by oil and diesel costs tied to the Middle East conflict.

The same energy shock that frustrated consumers all spring is now showing up at the factory gate.

On the trading floor, April was a celebration. On the factory floor, it was a warning.

Chart Of The Week: Factory Inflation Is Back — And Consumers Are Next

Photo: Shutterstock

Recent Comments