Something unusual happened Monday in the most beaten-down corner of the U.S. stock market.

Software stocks — down more than 30% from their late-2025 highs, written off by Wall Street as the collateral damage of generative AI commoditizing code — logged their best single session in more than a year, rising nearly 5%.

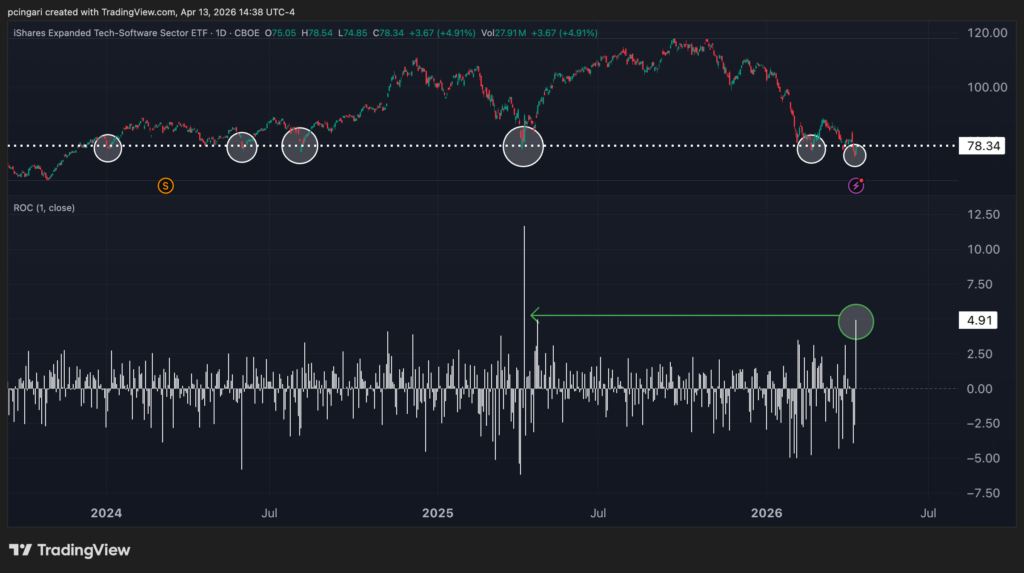

The iShares Expanded Tech-Software Sector ETF (NYSE:IGV) surged 4.9%, its strongest daily gain since April 8, 2025, the day markets exhaled after the Trump tariff panic.

Of 117 names in the ETF, 112 saw the green on the trading screen.

But the arithmetic of who actually drove the rally tells a more specific story.

One company provided 90 basis points of that 4.9% surge. By itself, that single name accounted for more than 20% of the entire sector’s daily move.

That company was Oracle Corp. (NYSE:ORCL) which jumped over 11%.

The IGV Had Already Broken Down

Context matters here. On Friday, April 10, the IGV closed at $74.67 — its lowest level since November 13, 2023.

That close wasn’t just a new multi-year low. It also confirmed a technical breakdown: the $76 support line that had held through five separate tests had finally given way.

Chartists were drawing conclusions. The bear software case felt like it was being confirmed in real time.

Monday’s 4.9% rebound didn’t erase that damage. But it injected enough ambiguity to force a reassessment.

The question isn’t whether one session reverses a six-month downtrend. The question is what catalyzed it — and whether that catalyst has legs.

What Happened To Oracle On Monday?

In the seven days leading up to April 13, the company had fired three distinct catalysts at investors in rapid succession.

On April 6, Oracle announced the appointment of Hilary Maxson as new chief financial officer, effective immediately.

Maxson came from Schneider Electric SE (OTC:SBGSF) , where she oversaw more than $45 billion in annual revenue and helped steer the company’s transformation into a software and AI energy platform.

The signal the market read: disciplined capital allocation at a company where cloud infrastructure demand is outpacing supply. Oracle’s most recent quarter delivered its strongest revenue growth in 15 years.

On April 9, Oracle unveiled Fusion Agentic Applications for HR — eight new AI-agent-powered products built into its existing cloud suite. The architecture was notable: these aren’t chatbot wrappers.

They are agentic systems designed to make and execute decisions within existing enterprise workflows, operating inside Oracle’s own security and compliance framework without requiring custom development.

Then on Monday morning itself, Oracle announced expanded AI capabilities across its Utilities Industry Suite — including AI-powered anomaly detection, GenAI asset summarization, and an affordability solution aimed at helping utilities manage arrears and regulatory pressure.

Oracle’s utilities platform already serves six of the top 10 largest U.S. utilities and helps deliver 2.8 billion customer bills annually across more than 60 countries.

The Software Leaderboard On Monday

Here’s how the top contributors to Monday’s IGV move stacked up, ranked by basis-point contribution to the ETF’s total return:

| Company | Price | Weight | Return | Contribution |

|---|---|---|---|---|

| Oracle Corp. | 153.70 | 8.30% | +11.31% | +89bps |

| Palantir Technologies Inc. (NASDAQ:PLTR) | 133.30 | 8.29% | +4.09% | +34bps |

| Salesforce, Inc. (NYSE:CRM) | 172.76 | 7.01% | +4.73% | +33bps |

| AppLovin Corp. (NASDAQ:APP) | 414.72 | 4.81% | +5.96% | +28bps |

| Microsoft Corp. (NASDAQ:MSFT) | 382.14 | 8.99% | +3.04% | +28bps |

| CrowdStrike Holdings, Inc. (NASDAQ:CRWD) | 401.11 | 4.39% | +5.83% | +25bps |

| Adobe Inc. (NASDAQ:ADBE) | 238.82 | 4.25% | +5.98% | +25bps |

| Cadence Design Systems, Inc. (NASDAQ:CDNS) | 286.22 | 3.32% | +7.74% | +25bps |

| ServiceNow, Inc. (NYSE:NOW) | 88.53 | 3.73% | +6.67% | +25bps |

| Palo Alto Networks, Inc. (NASDAQ: PANW( | 162.05 | 5.71% | +4.06% | +23bps |

The gap between Oracle and the rest of the field is stark.

The next largest contributor — Palantir Technologies Inc. — generated 34 basis points of contribution.

Oracle nearly tripled that.

Even though Microsoft Corp. carries the biggest weight in the ETF at 8.99%, its more modest 3% daily gain translated to just 28 basis points.

The question Monday’s session leaves unanswered: was Oracle’s 11% surge a company-specific re-rating triggered by a week of genuine catalysts — or is it an oversold bounce in a sector where the structural headwinds haven’t gone anywhere?

Whether Oracle becomes the reason software finds a floor, or simply the loudest voice in a dead-cat bounce, is a question the next few sessions will begin to answer.

Photo: Shutterstock

Recent Comments