Coinbase Global Inc. (NASDAQ:COIN) stated on Wednesday that its users can borrow USDC (CRYPTO: USDC) against their cryptocurrency holdings to cover tax bills, avoiding the need to sell them.

Coinbase Presents ‘Choice’ For Users

In an X post, Coinbase said that selling cryptocurrencies would trigger capital gains taxes and could create a cycle of selling more to cover the new taxes.

Remember that tax applies only when you realize the gains. Capital losses aren’t taxable.

The other option they suggested was to get loans in USDC while holding the cryptocurrency, including Bitcoin (CRYPTO: BTC) and Ethereum (CRYPTO: ETH), as collateral, with the loan itself not treated as a taxable event. Later, they can convert the USDC into dollars, pay taxes with that cash and keep their cryptocurrency bags intact.

On Coinbase, you can swap dollars for USDC and vice versa at a straightforward 1:1 rate, with no fees or tax implications in most cases.

Coinbase left it to users to decide, with an explicit disclaimer that this is not tax advice.

Hidden Risks?

Replies to the post flagged potential liquidation risks during market drops. Others warned that even slight fluctuations in USDC’s value against the dollar could trigger its own taxation.

Meanwhile, the Internal Revenue Service confirmed it will continue normal operations during the ongoing partial government shutdown, and the April 15 filing deadline for filing taxes will remain unchanged.

Price Action: Coinbase shares fell 0.11% in after-hours trading after closing 0.03% higher at $181.010 during Wednesday’s regular trading session, according to Benzinga Pro.

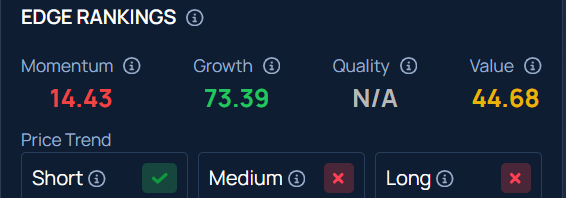

COIN stock lagged in medium- and long-term price performance but showed strength in the short term, according to Benzinga’s Edge Stock Rankings.

Photo: Bukhta Yurii / Shutterstock

Recent Comments