Euro-area forecasters had projected in February that officials at the European Central Bank (ECB) would resume cutting rates at the upcoming meeting this month.

What a difference a month can make. The US‑Israeli military operations against Iran, now in their second week, have upended the ECB equation, shaking the central bank’s “good place,” according to ING.

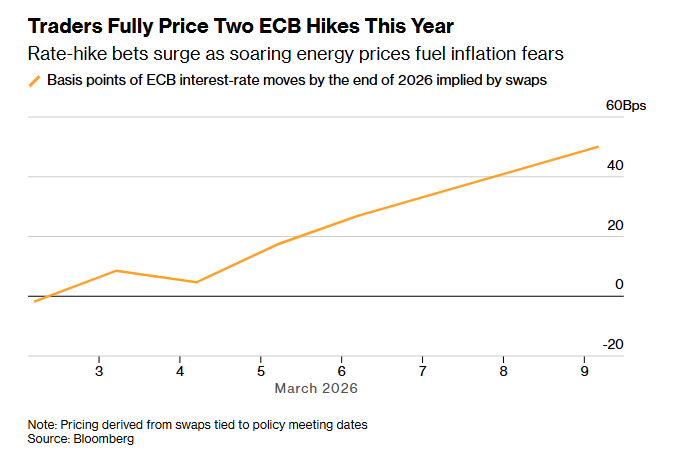

Traders have increased their bets on interest-rate hikes from the ECB after European natural gas prices doubled and Brent crude rose 26% since February 27, a day before the military operations began. Swaps imply around a 70% probability of two 25-basis-point rate increases by the ECB this year, up from the single move priced on Friday, Bloomberg reported.

Morgan Stanley on March 5 forecast that the ECB will keep interest rates steady through 2026, citing potential inflation risks due to the conflict in the Middle East. The Wall Street brokerage had previously anticipated two ECB rate cuts in June and September.

“At the current juncture, the risk of a wage-price spiral looks small,” ING’s Global Head of Macro, Carsten Brzeski, wrote on Wednesday. “Still, in a ‘forever war’ scenario of a longer-lasting disruption of the Strait of Hormuz, oil prices above $100/b for several months, and knock-on effects on transportation, food prices, and more generally supply chains, are likely to force the ECB’s hand and consider rate hikes.”

ECB Is a Beacon of Continuity

Before the outbreak of war in the Persian Gulf, where 20% of global energy flows, ING Think had said that “the ECB has almost become a beacon of continuity – some might even say boredom.” It added that the ECB remained comfortably in its “good place.”

Like Morgan Stanley, ING Think had expected at the end of January that the ECB would keep its rates unchanged for the rest of the year. It hedged its position by adding that the central bank’s policy would stay the same unless there were “strong positive or negative surprises to force the ECB back into action.”

The surprise attacks by the US and Israel, and the closure of the Strait of Hormuz, will pressure ECB officials to act when they meet from March 18–19. US President Donald Trump said operations would follow a four-week timetable after nearly two weeks of intense strikes.

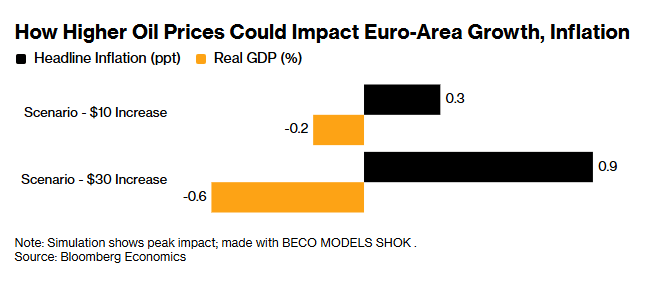

“The US-Israeli strike on Iran and Tehran’s retaliation have already sent oil toward $80 a barrel, from a pre-escalation average of $65,” Bloomberg economists Jamie Rush, Björn van Roye, and Ziad Daoud wrote. “European gas prices have also moved higher. Running these scenarios through our in-house economic model shows that CPI will be up and GDP down across major advanced economies, triggering conflicting impulses for central banks.”

Lagarde Says ECB to Keep Inflation Under Control

ECB President Christine Lagarde reiterated Tuesday that the central bank would take the necessary steps to keep inflation under control. The war risks forcing the ECB to raise interest rates sooner than anticipated, Governing Council member Peter Kazimir said.

“We will do all that is necessary to ensure inflation is under control and French and Europeans don’t suffer the same inflation increases like those we saw in 2022 and 2023,” Lagarde told France 2.

At its February monetary policy meeting, the ECB kept rates steady at 2%. Central bank officials emphasized that inflation was stabilizing near the 2% target with resilient economic growth and low unemployment at 6.2% in December.

“Geopolitical tensions, in particular Russia’s unjustified war against Ukraine, remain a major source of uncertainty,” Lagarde said at last month’s monetary meeting. “Inflation could turn out to be higher if there were a persistent upward shift in energy prices.”

Euro area annual inflation is expected to be 1.9% in February 2026, up from 1.7% in January, according to a flash estimate from Eurostat, the statistical office of the European Union (EU).

Officials Warn Against Rush to Cut Rates

Some European officials have cautioned against a rush to raise rates.

Italian Finance Minister Giancarlo Giorgetti warned, “It would be a grave problem to think that the solution could be monetary tightening.”

Growth in Italy eased to 0.5% in 2025 from a revised 0.8% the year before. Higher rates driven by the Middle East conflict could push the economy into more serious trouble.

Irish Finance Minister Simon Harris also told reporters that there’s a risk of inflation accelerating if the US and Israel enter into a prolonged conflict against Iran. He added that it’s currently hard to say how long the conflict will last.

“The inflationary impact of that could be very significant for whole swathes of the Irish economy, of the European economy, of the global economy,” he said. “We do need to take this step by step and day by day.”

Impact on Industries

The euro area’s economic condition appeared fragile even before the war, making the impact on European industries more likely. If the conflict goes on longer than predicted by US officials, the euro area will feel the fallout.

In December, seasonally adjusted industrial production decreased by 1.4% month-on-month in the euro area and by 0.8% in the EU, according to first estimates from Eurostat. In November 2025, industrial production grew by 0.3% in the euro area and fell by 0.1% in the EU.

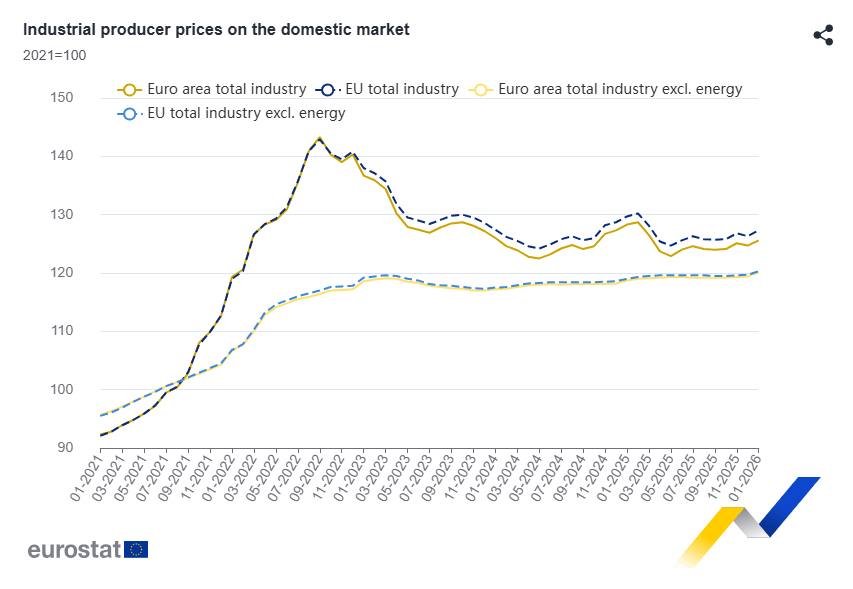

Industrial producer prices increased by 0.7% in the euro area and by 0.8% in the EU in January, compared with December, data from Eurostat showed.

The renewed weakness in industrial output adds another layer of pressure on the ECB, limiting its room to delay action if energy‑driven inflation accelerates.

“For the ECB, the war in the Middle East and rising energy prices are the intruders threatening Lagarde’s ‘good place,'” Brzeski wrote. “The key question for next week is what Lagarde and the rest of the Governing Council decide to do from inside their own panic room.”

He added that “one or two symbolic rate hikes could be enough to preempt any second-round effects and could strengthen the ECB’s inflation-fighting credibility.”

Disclaimer: Any opinions expressed in this article are not to be considered investment advice and are solely those of the authors. European Capital Insights is not responsible for any financial decisions made based on the contents of this article. Readers may use this article for information and educational purposes only.

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.

Recent Comments