Mastercard Incorporated (NYSE:MA) reported better-than-expected fourth-quarter financial results on Thursday.

The company reported quarterly net revenues of $8.81 billion, up 18% year-over-year and 15% Y/Y on a neutral currency basis, beating the analyst consensus estimate of $8.79 billion. Adjusted EPS rose 25% Y/Y to $4.76, exceeding the analyst consensus estimate of $4.25.

Mastercard expects net revenue growth in the low teens for the first quarter, versus the $8.3 billion analyst consensus estimate. The company expects high-end of low double-digit revenue growth for fiscal 2026 versus the $36.8 billion analyst consensus estimate.

Mastercard shares fell 1.3% to trade at $536.16 on Friday.

These analysts made changes to their price targets on Mastercard following earnings announcement.

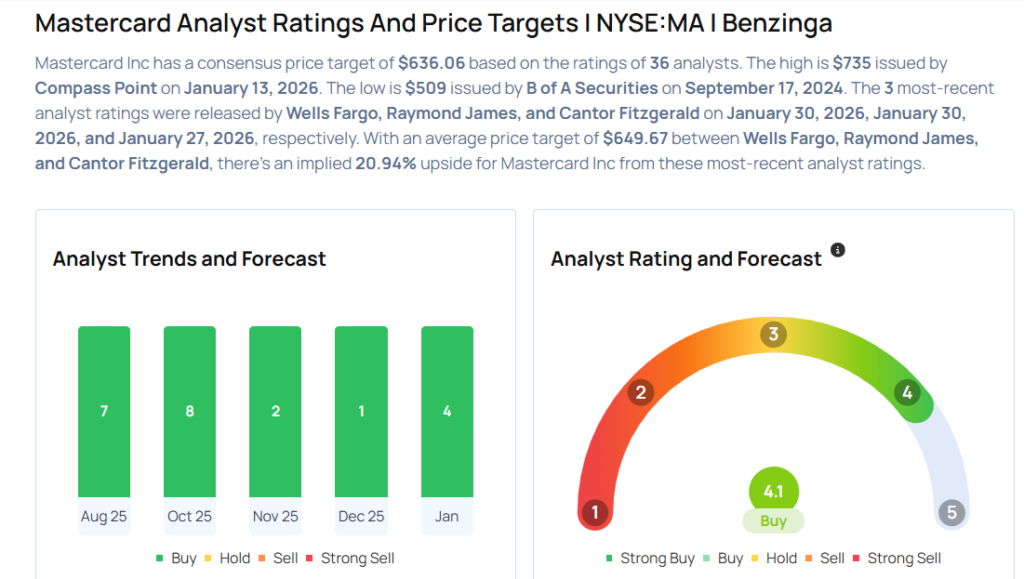

- Raymond James analyst John Davis maintained Mastercard with an Outperform rating and lowered the price target from $707 to $631.

- Wells Fargo analyst Jason Kupferberg maintained the stock with an Overweight rating and raised the price target from $660 to $668.

Considering buying MA stock? Here’s what analysts think:

Photo via Shutterstock

Recent Comments