Trade risk rises as earnings loom for mega caps

Tariff Anxiety Returns to the Tape

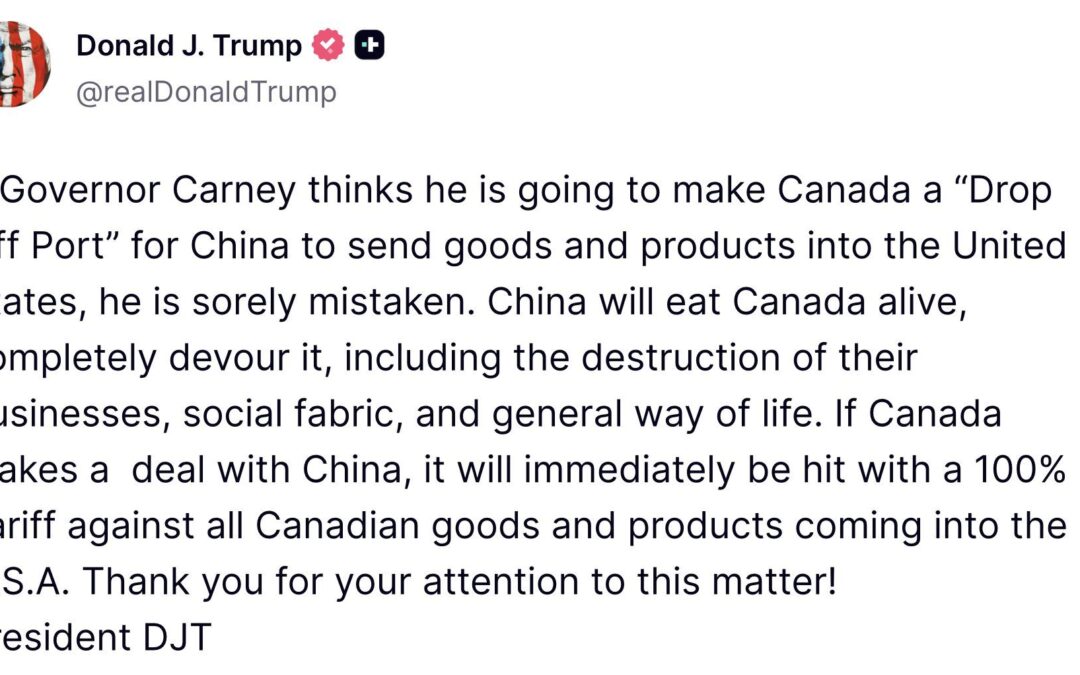

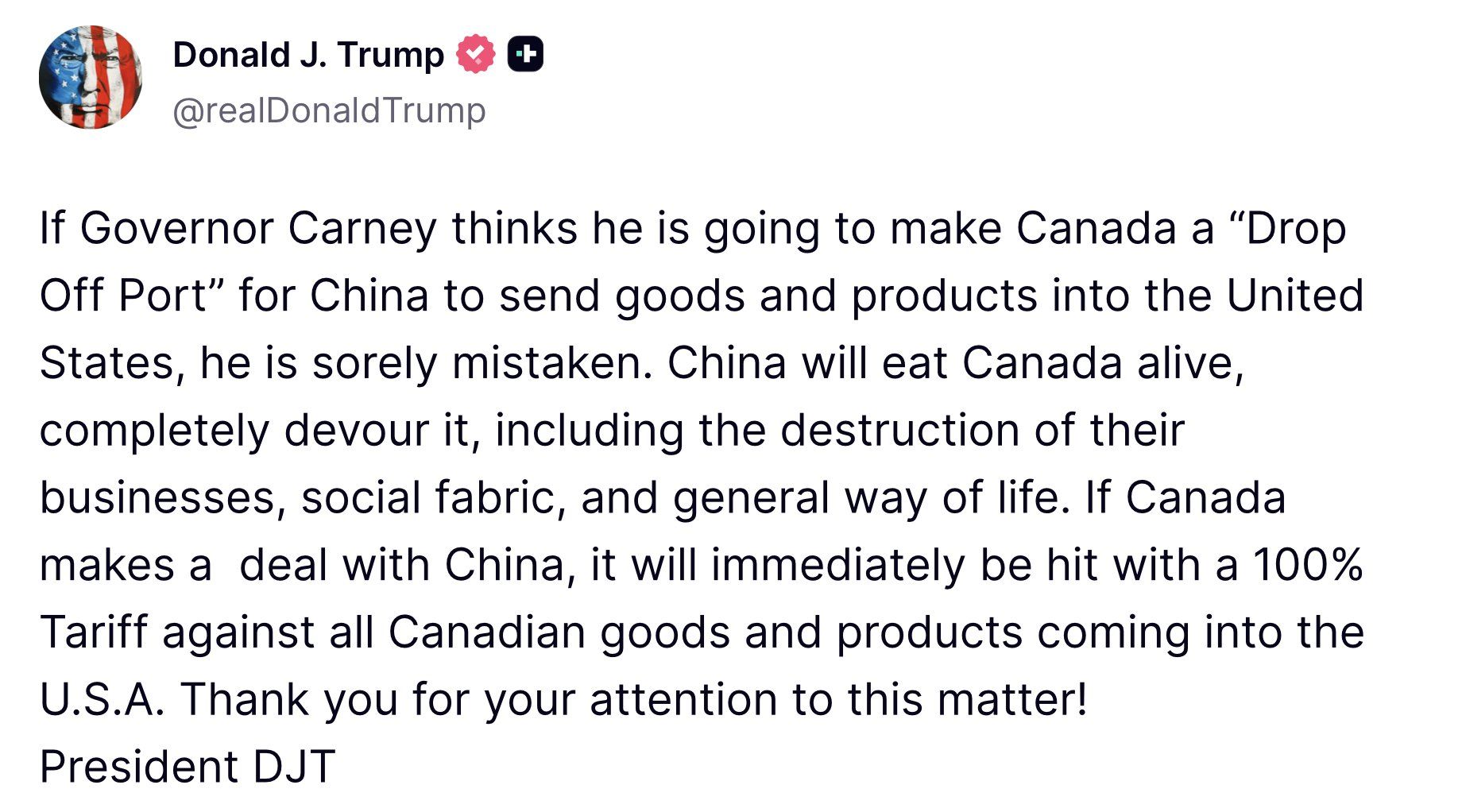

Renewed fears around a potential Canada-China deal are reviving concerns about additional U.S. tariffs. The issue is not confirmed policy, but positioning, markets remain sensitive to anything that reopens the trade front just as growth expectations stabilize. Even incremental headlines are enough to reprice risk across globally exposed sectors.

The sequencing matters. Trade narratives tend to surface when markets are extended, forcing fast adjustments across equities, FX, and rates. For now, this sits firmly in headline risk territory, but it is enough to cap near-term enthusiasm.

Bitcoin Slides Back to 86k as the Yen Firms

Bitcoin has pulled back to roughly 86k after trading near 96k, keeping the broader downtrend intact. Part of the pressure coincides with renewed strength in the Japanese yen, a classic signal of tighter global financial conditions and reduced leverage appetite. High-beta assets tend to feel this first.

Crypto continues to trade as a liquidity proxy. Until currency volatility eases and risk appetite improves, Bitcoin (CRYPTO: BTC) is likely to remain range-bound with sensitivity to macro shifts rather than narrative catalysts.

Earnings Week for Tesla, Microsoft, Meta, and Apple

This earnings week carries outsized weight with reports from Tesla (NASDAQ:TSLA), Microsoft (NASDAQ:MSFT), Meta (NASDAQ:META), and Apple (NASDAQ:AAPL). Expectations are high, not just on results, but on forward commentary around AI spending, margins, and consumer demand. Guidance, not beats, will likely drive the market reaction.

The broader setup is fragile. With macro uncertainty still elevated, strong execution can stabilize sentiment, while cautious outlooks could amplify volatility. This week is less about one quarter and more about confidence in 2026 trajectories.

Thanks for reading! For more updates throughout the week, follow @WOLF_Financial

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.

Recent Comments